Insurance AI Is Running Into The Oldest Underwriting Problem

TL;DR: Earnix's June 2026 insurance AI report says insurers are moving from AI experiments toward execution, but the business issue is less the model and more the operating data underneath it. For U.S. property-casualty carriers facing tighter 2026 margins, the winner is not the insurer with the flashiest AI demo. It is the insurer that can turn claims, pricing, underwriting, and governance data into faster, defensible rate decisions.

##What Earnix Is Really Pointing At In Insurance AI

The useful part of the Earnix 2026 Industry Trends Report is not that insurers like AI. Everyone knows that by now.

The sharper point is that Earnix frames the next phase around pricing, underwriting, customer engagement, regulation, and data quality, based on a global survey of 400 insurance executives. That is a more uncomfortable story.

It says insurance AI is leaving the slide deck and entering the rate desk.

That is where the economics get real. A model that recommends a price, renewal action, or underwriting exception has to survive actuarial review, compliance, state insurance rules, agent pushback, and customer behavior. In insurance, "almost right" can become a bad book of business.

##Why The Margin Backdrop Matters For U.S. P/C Carriers

U.S. property-casualty insurers are not adopting AI from a position of endless slack.

AM Best said the U.S. P/C industry had its strongest performance of the past decade in 2025, helped by pricing and investment income, but also warned that softer rate trends and claims-cost pressure could tighten margins in 2026. That is the real setup.

When pricing power fades, operational delay becomes expensive.

A carrier that spots loss-cost movement three months late is not merely "less digital." It is letting old rates sit inside new risk. The hidden cost shows up later as adverse selection, reserve pressure, or a renewal book that looks profitable until claims catch up.

#The model is not the only bottleneck

The practical bottleneck is usually dull:

- policy data that does not match claims data;

- legacy systems that cannot feed pricing teams cleanly;

- privacy and governance rules that slow model deployment;

- underwriting exceptions that live in email, spreadsheets, or branch habits;

- regulators who need an explanation, not just an output.

That is why the AI story belongs in a finance feed. It is about who can preserve underwriting margin when rate actions get harder.

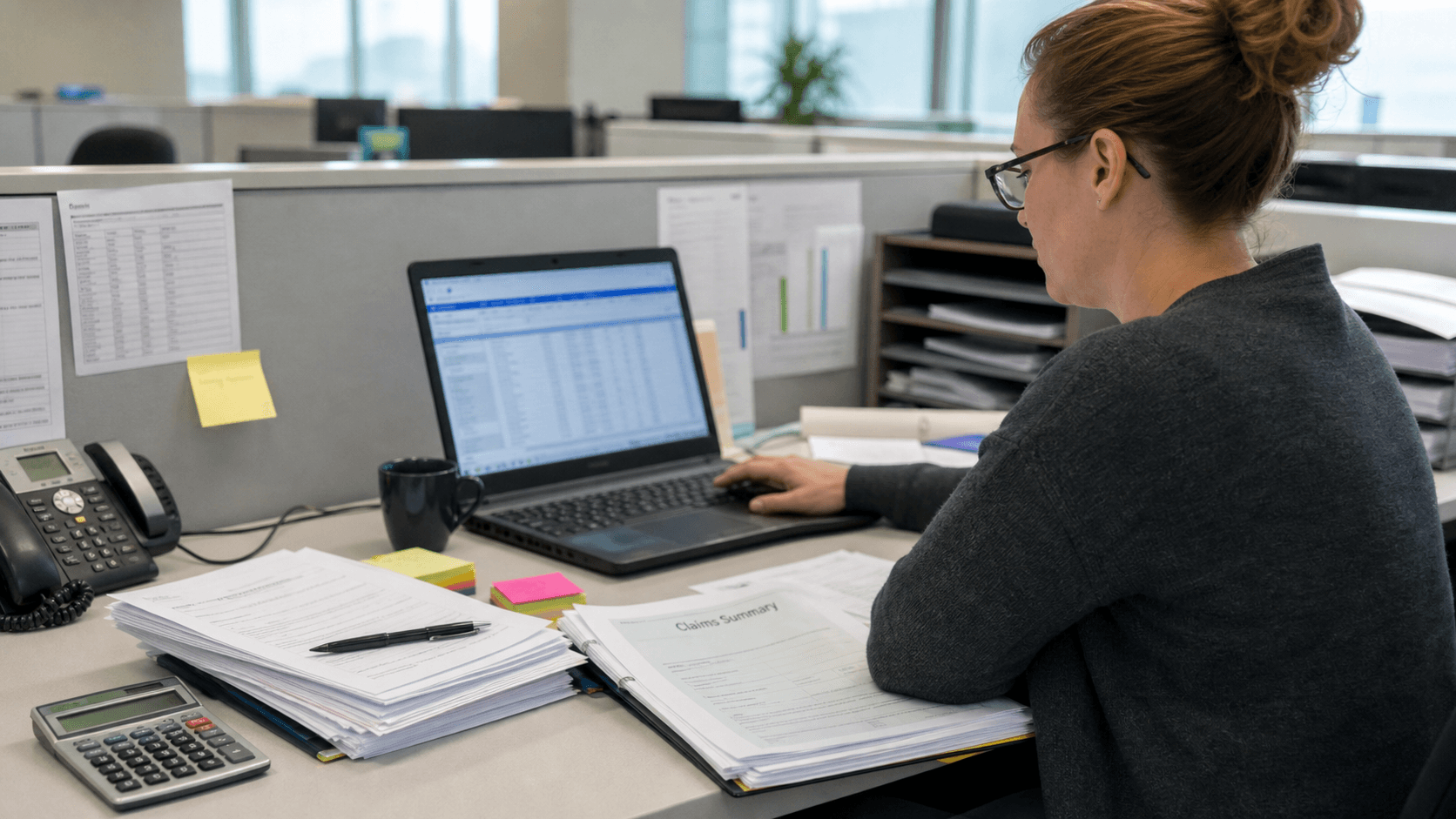

##Where The Work Actually Happens

Picture a pricing analyst at a P/C carrier reviewing an auto or homeowners book after repair costs move again.

The analyst has a claims summary, a renewal report, an actuarial indication, and a compliance checklist. The executive question sounds simple: should the carrier push price, tighten underwriting, change segmentation, or tolerate lower margin to keep customers?

AI can help with that decision only if the underlying data is current, traceable, and usable. If the data is fragmented, the model becomes another opinion in a room already full of opinions.

That is the part casual AI coverage misses. Insurers do not just need smarter recommendations. They need recommendations that can be defended when a regulator, reinsurer, CFO, or distribution partner asks how the decision was made.

#Good data changes speed, not just accuracy

The finance value is not only a better loss ratio forecast.

The value is a shorter loop between claim emergence, pricing action, product design, and renewal behavior. A carrier that can move that loop faster can protect margin without swinging blindly at every policyholder.

That matters because insurance pricing is a timing business. Move too slowly and the book deteriorates. Move too bluntly and profitable customers leave.

##Who Benefits If Insurance AI Becomes Boring Infrastructure

The obvious winners are software vendors that sell pricing, rating, underwriting, governance, and decisioning tools.

The less obvious winners are carriers with disciplined data plumbing. They can use AI to make existing operating routines sharper instead of building a parallel experiment beside the real business.

Investors should watch for three signs:

- management talks about rate adequacy and claims trends in the same breath as data infrastructure;

- AI projects connect to underwriting profit, expense ratio, retention, or cycle time;

- governance is treated as a deployment enabler, not a legal speed bump.

The laggards will describe AI as transformation while still pricing from disconnected systems.

##What The Market May Be Underpricing

S&P Global Market Intelligence data reported by Carrier Management showed a very strong first-quarter 2026 underwriting result for U.S. P/C insurers, with a combined ratio before policyholder dividends of 89.5. That kind of number can make the industry look healthier than its next operating problem.

But good recent margins can hide the urgency of the next cycle.

If repair costs, casualty severity, commercial competition, or weather losses move against carriers, the AI question will stop being "who has a chatbot?" and become "who can update the book without losing control of the process?"

That is a less glamorous question. It is also the one that affects earnings.

##The Gainbrief Takeaway

Insurance AI will not be won in a demo room. It will be won in the messy middle where underwriting, actuarial, claims, compliance, and finance all need the same version of the risk.

The best carriers may not look the most futuristic. They may simply close the loop between data and price faster than competitors.

In a tighter margin year, that is enough of an edge.

#FAQ

Why does insurance AI matter for investors?

Because AI in insurance can affect underwriting margin, expense ratios, retention, and pricing speed. Those are financial variables, not just technology features.

What is the biggest execution risk?

The biggest risk is weak data infrastructure. If claims, policy, pricing, and governance data do not connect cleanly, AI recommendations may be slow, hard to defend, or commercially unsafe.

Is this mainly a vendor story?

No. Vendors may benefit, but the more important story is carrier discipline. Insurers with cleaner operating data can convert AI into pricing power; insurers with fragmented systems may only add another layer of complexity.