Marvell Says the AI Bottleneck Is Moving Into the Network

Marvell's May 27 quarter says the AI infrastructure trade is no longer just about who can buy the most GPUs. The more interesting money is moving into the middle mile: custom chips, optical links, switches, and the boring data-center plumbing that decides whether expensive accelerators sit busy or wait on traffic.

That is a sharper signal than another "AI demand is strong" headline. Marvell reported record fiscal first-quarter 2027 revenue of $2.418 billion, up 28% from a year earlier, and guided second-quarter revenue to $2.7 billion at the midpoint, implying 35% year-over-year growth. The business case is simple: once hyperscalers commit to enormous AI factories, they cannot afford weak connective tissue.

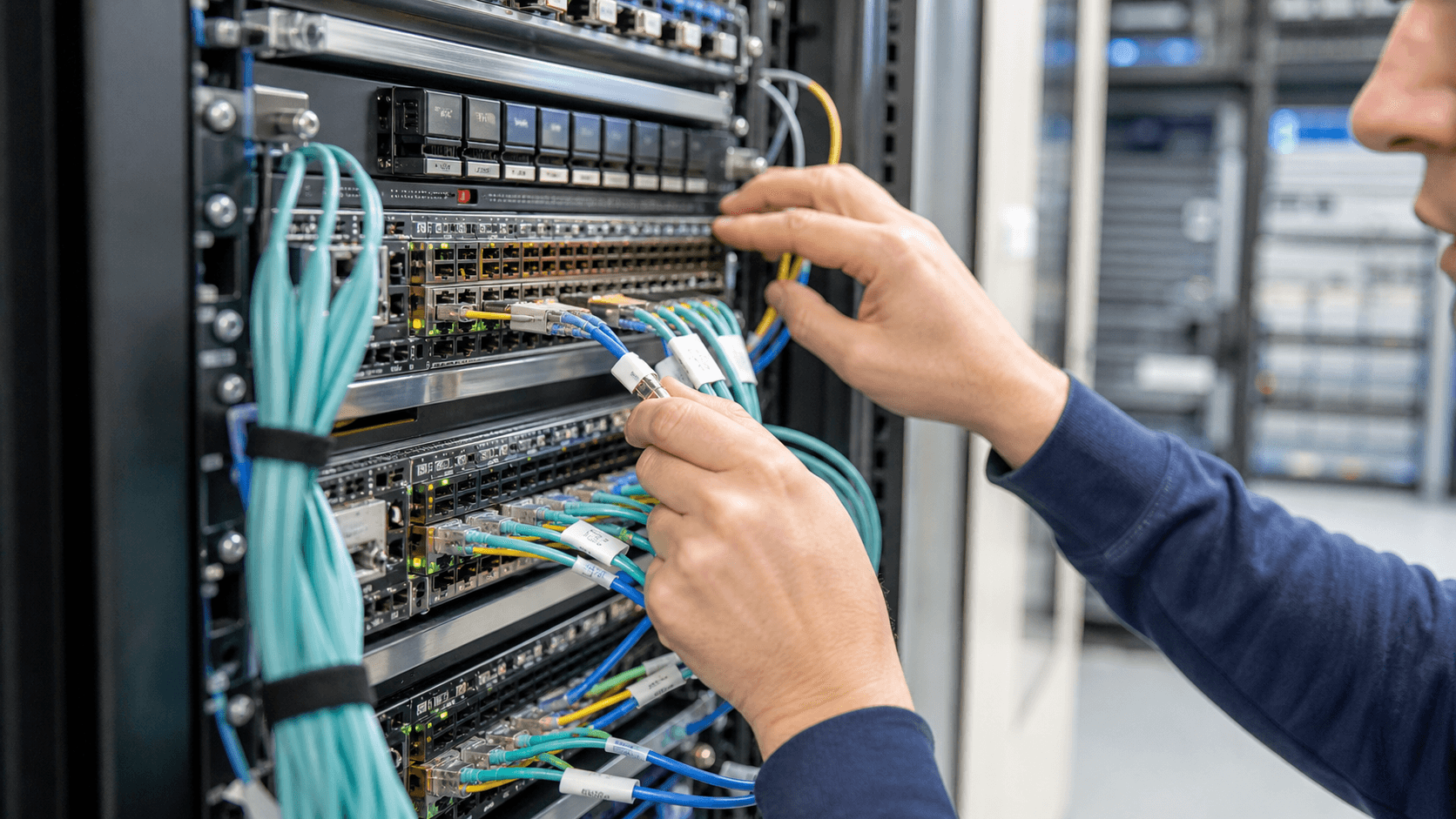

By the third rack row in a data center, the GPU story turns physical. A technician is not staring at a chatbot demo. She is tracing cables, optics, heat, power, and packet flow. One wrong constraint can turn a very expensive cluster into an underused warehouse.

That is why Marvell matters right now. The company sits in the less glamorous layer between the famous accelerator and the customer invoice. It sells the silicon and networking pieces that help cloud operators and AI builders move data fast enough for training and inference workloads.

The market likes to talk about compute as if it were one object. It is not.

AI infrastructure has at least three separate businesses hiding inside the same spending boom:

- The chip vendor that sells the accelerator.

- The cloud or AI operator that rents the capacity.

- The networking and custom-silicon supplier that keeps the system from choking.

The third business is easy to underrate because it does not look heroic on a slide. It looks like throughput, latency, optics, board design, firmware, procurement timing, and supply assurance.

But that is exactly where a new profit pool can form.

Nvidia's own May report made the same point indirectly. Nvidia posted $81.6 billion of first-quarter fiscal 2027 revenue, including $75.2 billion from Data Center, and said Data Center networking revenue reached $14.8 billion, up 199% from a year earlier. When networking grows faster than the headline data-center number, the message is not subtle.

The AI factory is becoming a network economics problem.

Marvell is not trying to be Nvidia. That is the wrong frame. Marvell is trying to be one of the companies that makes the customer's Nvidia-heavy or custom-accelerator-heavy buildout usable at scale.

That distinction matters for investors because the AI capex debate is becoming too binary. Either the whole boom is a bubble, or every supplier with "AI" in the sentence deserves a premium. Both views are lazy.

The better question is: which suppliers become harder to remove as clusters get larger?

Custom silicon and optical interconnects can become sticky because they are designed into a system before the system produces revenue. Once a hyperscaler standardizes a design, the switching cost is not just a new purchase order. It can mean retesting, redesigning boards, changing power and cooling assumptions, and risking delivery schedules.

That is not software-style lock-in. It is schedule lock-in.

Picture a procurement meeting at a cloud company after a major AI customer asks for more capacity. The CFO does not care whether the winning component has the best origin story. The question is whether the next cluster comes online in time, runs near full utilization, and avoids a margin leak from idle equipment.

In that room, the supplier selling reliability into the build schedule has more power than the supplier selling a generic part.

Marvell's latest guidance points to that reality. Management said it expects revenue growth to keep accelerating through fiscal 2027, driven by data-center strength and exceptional AI-related bookings. That wording matters because bookings are not applause. They are customers reserving a place in a complicated supply chain.

The twist is that AI infrastructure may be getting less like the old chip cycle and more like a construction backlog.

In a normal semiconductor cycle, investors obsess over units, inventory, and pricing. In this cycle, the more important question may be whether the customer can build a working factory quickly enough to monetize the hardware already promised. The constraint migrates from chip availability to system delivery.

That migration changes who gets paid.

If the bottleneck is raw accelerator supply, Nvidia captures the drama. If the bottleneck is cluster utilization, then networking silicon, optics, custom accelerators, power gear, and integration partners become more important. Not all of them win equally. But the category deserves more attention than it gets.

There is still risk. Marvell is tied to a concentrated group of data-center buyers. AI spending could slow. Custom programs can slip. Margins can disappoint if the company has to scale too quickly or if hyperscalers use their buying power aggressively.

But the important part is not that Marvell had a good quarter. The important part is that the AI buildout is becoming harder to analyze from the top of the rack.

The next phase will not be decided only by who owns the fastest chip. It will be decided by who owns the traffic pattern, the custom design slot, and the delivery calendar. That is a quieter business than the GPU trade, but quiet is not the same thing as small.

The next AI margin question may be hiding in the cables.