The AI Chip Boom Is Learning to Charge for Uptime

The AI chip boom is no longer just about selling one more machine into one more fab.

It is starting to become a business of selling fewer bad wafers, fewer surprise shutdowns, and fewer hours of expensive equipment sitting there slightly wrong.

That is the part of the trade I think a lot of investors still underweight.

Reuters reported on May 21 that Lam Research plans to add more sensing and AI capabilities to its chipmaking tools, while expanding around Phoenix and investing further in Fremont. On the surface, that sounds like a standard "AI helps optimize operations" headline.

It is more important than that.

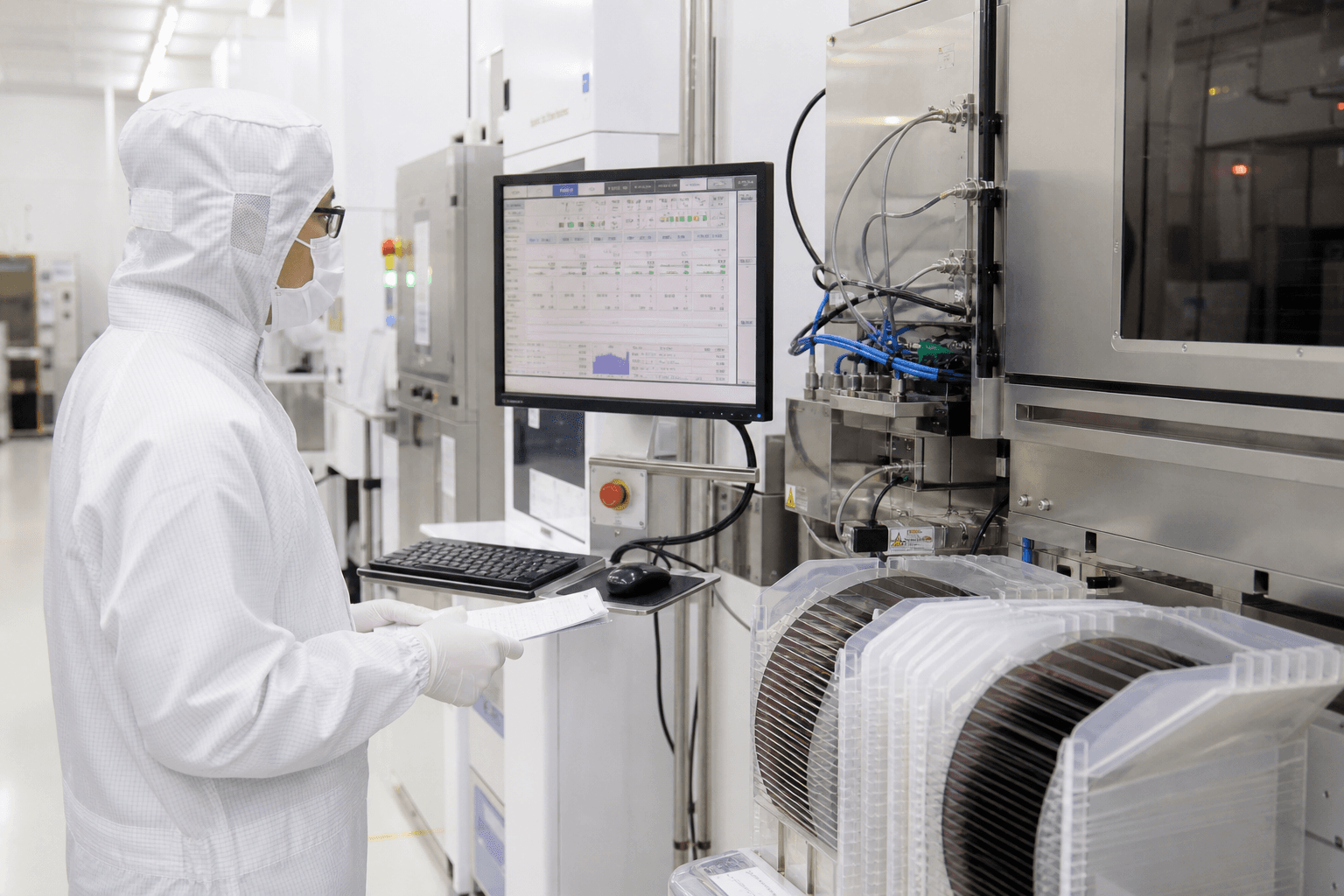

Picture the real scene. A process engineer is standing beside an etch tool, not in front of a PowerPoint, looking at a machine that already costs a fortune, already has a backlog behind it, and already sits in a factory where every delay can ripple through customer commitments. In that world, the next big win is not always buying another box. It is teaching the existing box to see trouble earlier.

That changes the economics of the semiconductor equipment business.

For the last stretch of the AI boom, the easy story was capacity. More GPUs meant more wafers. More wafers meant more deposition, etch, inspection, packaging, and cleanroom build-out. Everyone could understand that trade.

The harder story is productivity.

Lam's CEO told Reuters the company wants more sensors on its tools so AI systems can catch problems and inefficiencies earlier, helping customers produce more good chips with fewer defects. Lam even highlighted a startup working on shrinking a chip-measurement step so it can be embedded into an existing machine instead of requiring a separate one.

That sounds like an engineering detail. It is really a margin story.

Lam reported March-quarter revenue of $5.84 billion, up 9% from the prior quarter, with operating margin at 35.0%. More interestingly, customer support-related revenue was about $2.11 billion, more than a third of total revenue. That line includes service, spares, upgrades, and non-leading-edge equipment.

In other words, the fab-tool business is already not just a hardware shipment business.

If AI makes those tools better at prediction, diagnosis, and self-correction, the most valuable part of the relationship may shift even further toward upgrades, software-like improvements, and service intensity. The customer is not just buying a machine. The customer is buying yield insurance.

That matters because the AI build-out is getting more crowded and more expensive at the same time.

SEMI said in April that worldwide 300mm fab equipment spending is expected to rise 18% to $133 billion in 2026. That kind of spending creates a temptation to treat every winner as a pure volume beneficiary. But once fabs are this full of expensive equipment, the next bottleneck is not only supply. It is coordination, uptime, and defect control.

That is why Lam opening another Phoenix-area facility near TSMC matters more than the building itself. Support moves closer to the fab because the value is moving closer to the workflow. If the money were only in selling the original machine, you would care mostly about the purchase order. If the money is increasingly in keeping that machine productive, you care where the engineer, parts, and data loop sit.

This is also where the AI narrative gets more durable.

A lot of AI spending stories depend on hyperscalers, one-time server orders, or the next giant cluster announcement. Tool productivity is different. Once a chipmaker learns that better sensing and predictive models can lift yield or catch drift early, that behavior becomes operational, not promotional.

It turns AI from a capex event into a maintenance religion.

That has two consequences.

- First, semiconductor equipment makers may deserve to be valued less like cyclical box shippers and more like hybrid infrastructure suppliers with recurring support leverage.

- Second, the real competition inside AI manufacturing may move from who can deliver the most tools to who can make the installed base think harder.

The second point is the one I would watch.

If every advanced fab is stuffed with expensive machines, the winner does not automatically become the company with the biggest footprint. It may become the company that can turn a noisy factory into a more legible one.

That is a subtler business than the classic chip arms race. It is also stickier.

The next phase of the AI semiconductor boom may not be about who sells more metal into the fab. It may be about who gets paid to make the metal less blind.