McKesson's Apollo Deal Turns Medical Supplies Into IPO Prep Work

TL;DR: McKesson said on June 2 that Apollo closed a $1.25 billion convertible preferred investment for about 13% of Medical-Surgical Solutions at a roughly $13 billion enterprise value. The revealing part is not that private capital likes healthcare. It is that a medical-supply distribution unit is being groomed like a standalone financing asset before an IPO.

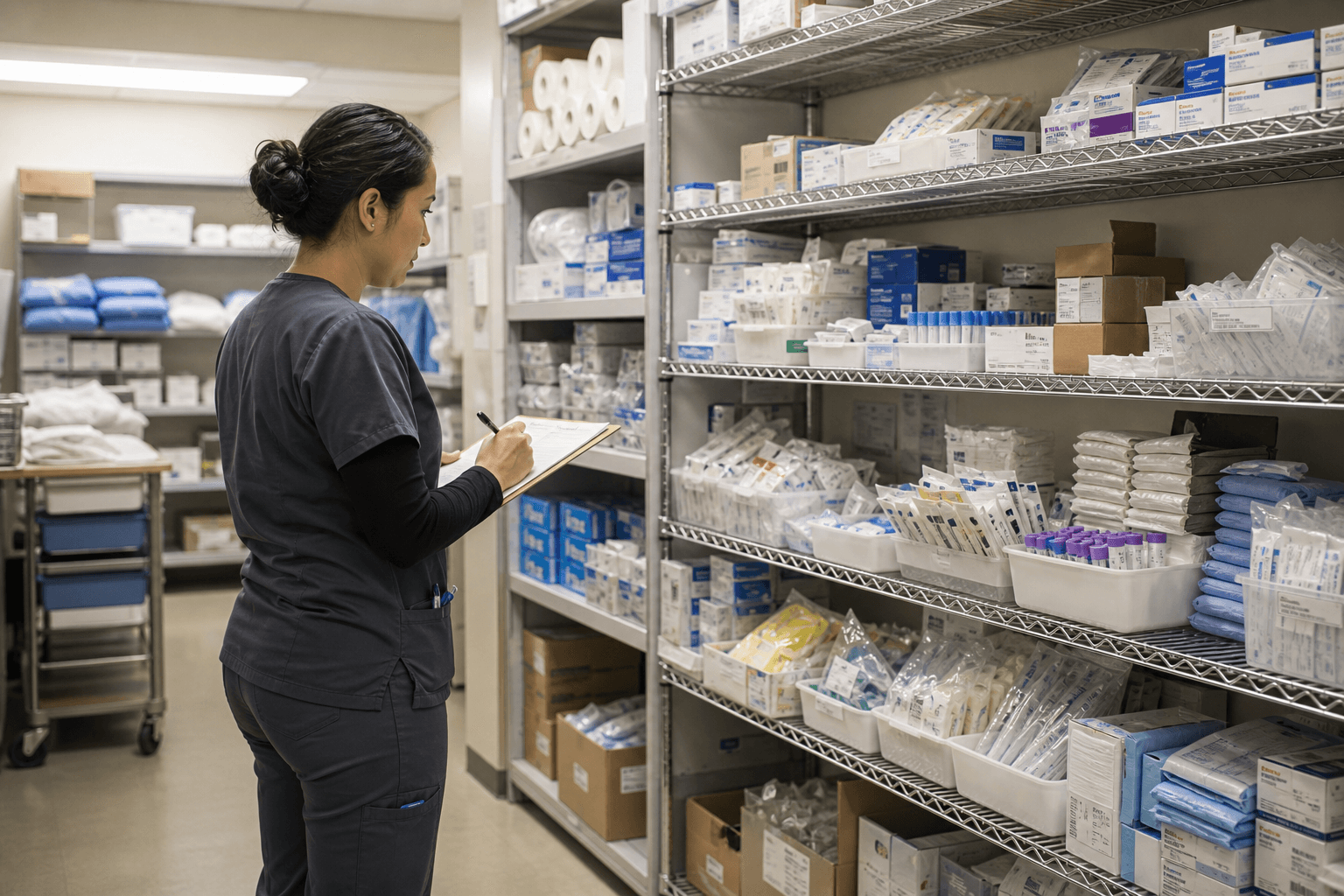

Walk into an outpatient clinic and the glamorous part of healthcare is nowhere in sight. You see exam-room paper, gloves, syringes, specimen kits, carts, monitors, reorder screens, and a back room that has to stay full without getting too full.

Walk into the banker version of that same story and you see the same business translated into different nouns: carve-out, preferred equity, term loan, revolver, valuation, separation, and public-market readiness.

That second room is where this story actually lives.

#The Supply Closet Is Being Marked To Market

McKesson announced in April that Apollo would invest $1.25 billion in convertible preferred equity for an approximately 13% minority stake in Medical-Surgical Solutions, valuing the business at about $13 billion. On June 2, McKesson said the investment had closed on June 1 and called it a key milestone toward separating the unit into an independent public company.

That is more informative than it sounds.

Medical-surgical distribution is usually treated like necessary plumbing. It moves products into physician offices, surgery centers, labs, and other non-acute settings. Important business, yes. Sexy business, no.

When a company can raise a strategic minority check against that asset before an IPO, the message is that the market sees something sturdier than routine distribution. It sees a business with cash flow that can be isolated, capitalized, and sold with a cleaner story.

#Why Apollo matters less as a buyer than as a signal

Apollo is useful here not because it discovered healthcare supplies. Apollo is useful because it is comfortable underwriting businesses that sit between operating company and financing product.

McKesson's April announcement explicitly said Apollo's experience with complex carve-outs and public-market transactions would help position MMS for separation. Read that again and strip away the corporate polish. Apollo is not just funding growth. It is helping validate the packaging.

#This Is IPO Prep Disguised As Partnership

The usual spin story is focus. Management says a business will run better on its own, get a purer multiple, and attract investors who actually want that exposure.

That is part of this case. It is not the whole case.

McKesson's May 7 full-year release said it had already completed initial financing transactions for the planned separation, including a $1.0 billion term loan and a $1.0 billion revolving credit facility. That means the business is not simply being narrated into independence. It is being fitted with the financing hardware of independence.

This is why the June 2 closing matters. The Apollo check is not random capital arriving at a healthy asset. It is a rehearsal for public ownership.

The real product being assembled here looks like this:

- a carve-out with a pre-priced minority stake,

- a segment already carrying standalone financing,

- and an IPO story built around dependable supply-chain relevance outside the hospital.

That combination tells investors what management wants them to believe before a prospectus does: this is not a sleepy side unit, but a financeable platform.

#What McKesson Is Really Selling

McKesson still keeps operating control and majority ownership, and it will continue to consolidate the results for financial reporting. That matters because the company is trying to do two things at once.

First, it wants to prove that Medical-Surgical Solutions deserves a more legible valuation than it gets as one piece inside a larger healthcare-services company.

Second, it wants to extract that value without losing strategic flexibility too early.

Those goals are related, but they are not identical.

#The hidden bet is on ordinariness

Investors often overpay for dramatic growth and underappreciate ordinary process businesses that customers cannot easily remove. The appeal of this unit is not moonshot technology. It is repeat behavior.

Clinics reorder. Surgery centers restock. Labs need consumables on time. Non-acute care does not work if basic supplies arrive late, in the wrong quantity, or with unreliable service.

That kind of ordinariness can become valuable in capital markets because it is easier to model, easier to lever, and easier to compare. The more predictable the workflow, the easier it is to turn "boring" into "defensible."

#Why This Matters Beyond McKesson

Casual readers may look at this and see another private-capital cameo in healthcare. The better read is that public companies are still searching for ways to separate dependable operating cash flow from messy conglomerate perception.

If the market rewards this path, more companies will try to float distribution, services, and workflow-heavy units as standalone stories with cleaner capital structures and narrower investor audiences.

That would be a subtle change in how healthcare businesses get valued.

The market used to reserve premium carve-out treatment for obvious growth engines or high-tech platforms. Deals like this suggest there is another category now: operationally dull, financially legible businesses that can be sold as resilient infrastructure for fragmented care settings.

That does not make the IPO inevitable or the valuation permanent. McKesson itself warns the separation is still subject to conditions and may not happen on the expected timeline.

But the June 2 close still tells you something important. Wall Street is willing to look at a supply closet and see issuance capacity.

#FAQ

What happened on June 2, 2026?

McKesson said Apollo closed its previously announced $1.25 billion investment for about a 13% interest in Medical-Surgical Solutions, confirming the transaction had moved from announcement to completed financing.

Why is this more than a routine healthcare investment?

Because McKesson is using the deal as part of a planned separation and future IPO. The transaction helps price the asset, validate outside demand, and show that the business can carry standalone financing before it trades on its own.

What should investors watch next?

Watch whether McKesson keeps building standalone disclosure and financing around Medical-Surgical Solutions, and whether the eventual IPO pitch frames the unit as a simple distributor or as infrastructure for non-acute care workflows.