Citi's 8,100 S&P 500 Call Turns AI Spending Into An Earnings Test

TL;DR: Citi raised its 2026 S&P 500 target to 8,100, citing an AI-driven earnings surge, just after a sharp tech-led selloff reminded investors how fragile that bet is. The business implication is simple: the AI trade is moving from multiple expansion to earnings delivery. If data-center spending cannot show up as real revenue, margins, and cash flow across the index, the market’s favorite story becomes a concentration risk.

##What Citi's 8,100 S&P 500 Target Is Really Saying

Citi lifted its year-end 2026 S&P 500 target to 8,100, up from 7,700, with strategist Scott Chronert pointing to an AI-led earnings surge.

That is not just a bullish index call. It is a very specific wager on the income statement.

For the last two years, investors could buy the AI theme on narrative: faster chips, larger models, more cloud demand, bigger capital budgets. The next leg is less forgiving. It asks whether all that spending can turn into enough profit to justify the S&P 500 already leaning hard on a small group of technology and semiconductor names.

The better question is not whether AI is important. It obviously is.

The question is whether AI can carry an index.

##Why The Timing Matters After A Tech-Led Selloff

The market had just shown the weak spot. On June 5, the S&P 500 fell 2.6% to 7,383.74, while the Nasdaq composite dropped 4.2%, with large technology stocks weighing on the tape after a strong jobs report pushed rate anxiety back into view.

That matters because a higher-rate backdrop changes the AI trade’s required proof.

When money is cheap, investors can forgive long payback periods. When yields are rising, a data center is not a vision statement. It is a capital project with financing costs, power needs, depreciation, supplier bottlenecks, and customer demand that must arrive on schedule.

#What changes when rates stop helping?

The same AI spending plan looks different when the discount rate moves against it.

A hyperscaler can still order chips. A cloud customer can still test new AI features. An enterprise CIO can still approve a pilot. But public-market patience narrows when the revenue ramp is slower than the capex ramp.

That is the hinge in Citi's call. The upside case needs AI earnings to be episodic in the good sense: sudden, visible, and large enough to reset estimates. The downside case is also episodic: one high-profile miss can make investors reprice the entire spending chain.

##Where The AI Earnings Test Shows Up First

Look at the desk, not the keynote.

Inside a real investment office, the AI trade is no longer a single stock chart on a monitor. It is an index worksheet. Portfolio managers are asking how much of their S&P 500 exposure is actually a bet on AI chips, cloud capex, networking gear, power capacity, and software monetization.

That is why Broadcom's latest report landed so loudly. Reuters reported via Investing.com that Broadcom shares fell after its second-quarter sales and AI chip forecast disappointed lofty expectations, even though management still described strong long-term demand.

Broadcom's own second-quarter release said AI semiconductor revenue reached $10.8 billion, up 143% year over year. In a colder market, that would sound absurdly strong. In this market, investors asked whether it was strong enough.

That is the new standard.

##Who Pays If The AI Capex Cycle Slows

The obvious losers in a failed AI earnings wave are chip and hardware stocks. The less obvious losers are the companies that quietly built their 2026 margin story around AI eventually lowering unit costs or lifting revenue per employee.

The handoff points are easy to miss:

- Cloud providers pay first through capital expenditure, depreciation, and power contracts.

- Semiconductor and networking suppliers book the early revenue, but inherit forecast pressure.

- Enterprise software vendors must prove AI features can support pricing, not just demos.

- Index investors absorb the concentration risk when the same names drive both earnings optimism and selloff pressure.

This is why an index target can become a business-model story. AI optimism is no longer sitting outside corporate finance. It is inside budgets, vendor contracts, energy planning, and shareholder return math.

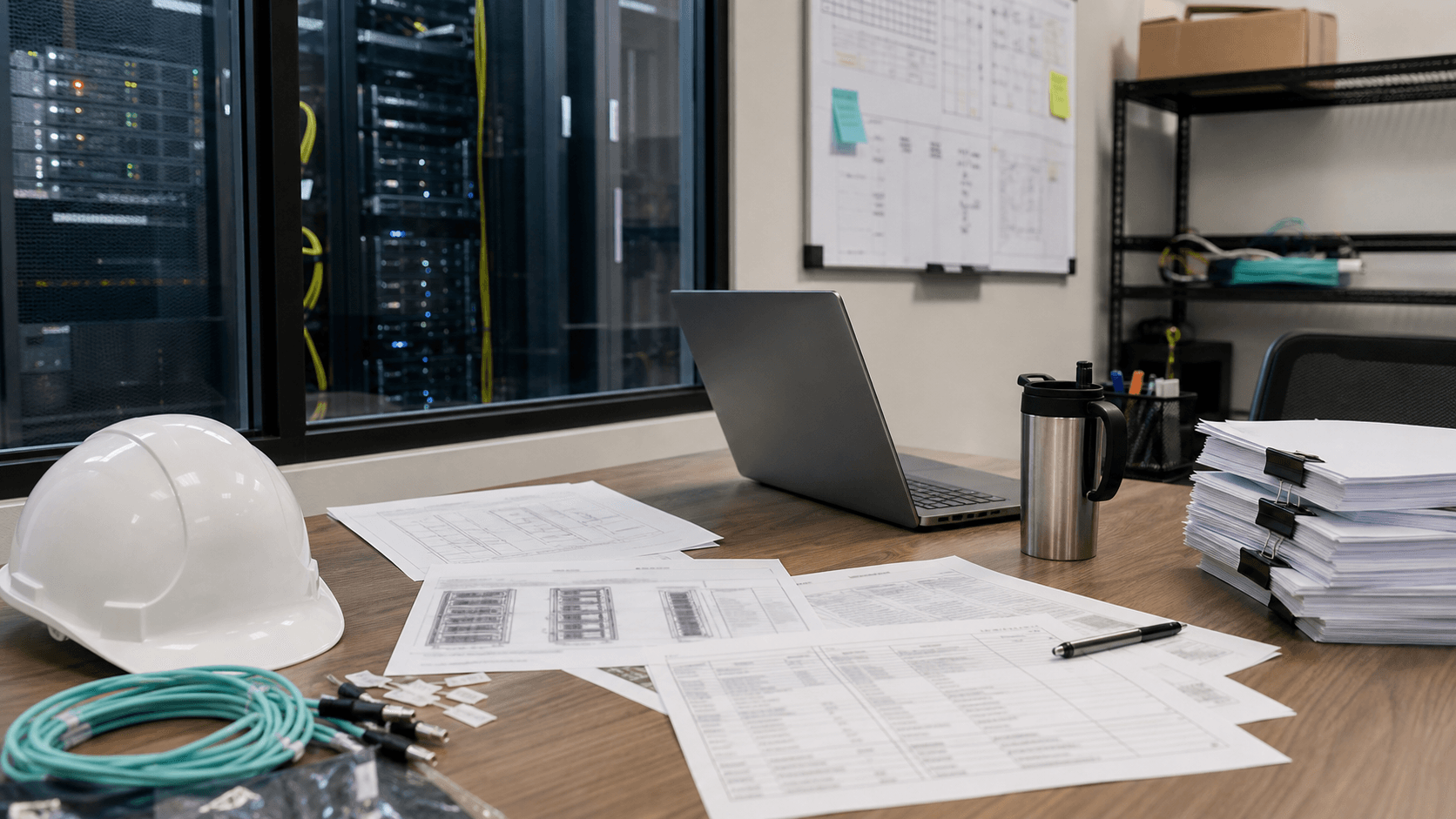

#The procurement scene is the market story

Picture a data-center procurement desk with rack diagrams, vendor invoices, and a laptop open beside a server room window.

That desk is where the S&P 500 target becomes real. Someone has to commit capital before the earnings show up. Someone has to secure components before the revenue is booked. Someone has to explain to investors why depreciation is rising faster than the product line that is supposed to pay for it.

The market is not short of belief. It is short of clean payback evidence.

##What Investors Should Watch Instead Of The Headline Target

The 8,100 number will get attention because index targets are easy to clip and argue about. The more useful signal is how quickly AI spending migrates from capital intensity to operating leverage.

Watch three things.

First, whether suppliers like Broadcom can keep turning AI backlog into revenue without resetting expectations every quarter.

Second, whether hyperscalers can show that data-center spending is supporting higher-value cloud revenue, not just defending strategic position.

Third, whether non-chip companies can use AI to improve margins in ways that are visible below the revenue line.

If those three pieces line up, Citi's call will look less aggressive than it sounds. If they do not, the S&P 500 will not merely have an AI problem. It will have an earnings-quality problem disguised as an AI problem.

##The Twist

The market's AI debate still sounds like a technology debate. It is becoming an accounting debate.

That is less exciting, but more important. The next serious AI surprise may not come from a model demo or chip launch. It may come from a quarterly report where depreciation, capex, pricing, and customer adoption finally agree with each other.

Until then, 8,100 is not a forecast. It is a receipt the market has not earned yet.

#FAQ

Why does Citi's S&P 500 target matter for investors?

It signals that a major Wall Street strategist sees AI-driven earnings as strong enough to lift the broader index. The risk is that the index has become more dependent on a narrow set of AI-linked companies delivering on that earnings promise.

Is this just another AI stock story?

No. The better angle is financial: AI infrastructure spending must now move through capex budgets, supplier revenue, depreciation, software pricing, and index-level earnings estimates. That makes it a market-structure and corporate-finance story, not just a technology story.

What could break the bullish AI earnings case?

The case weakens if chip demand stays strong but hyperscaler payback slows, enterprise AI revenue remains small, or higher rates make long-dated infrastructure spending harder to justify. The market can believe in AI and still reject the timing of the profits.