IREN's Dell Order Turns AI Demand Into a Delivery Clock

IREN's new $1.6 billion Dell order is not just another AI infrastructure headline. It is a reminder that the AI trade is moving from "who has demand?" to "who can turn hardware, power, installation, warranties, and financing into usable compute on schedule?"

That is the overlooked business story. In AI cloud, time-to-compute is becoming a financial asset. A GPU sitting in a supplier queue is a promise. A GPU commissioned at a data center in Childress, Texas, is revenue capacity.

IREN said on May 26 that it entered a purchase agreement with Dell Technologies for air-cooled Nvidia Blackwell systems. The order is meant to support IREN's previously announced five-year, $3.4 billion managed-services AI cloud contract with Nvidia. The company says commissioning at its Childress campus is targeted for early 2027.

The market likes the simple version: more GPUs, more AI revenue, bigger infrastructure story.

The sharper version is less glamorous. IREN is turning into a delivery company with a very expensive stopwatch.

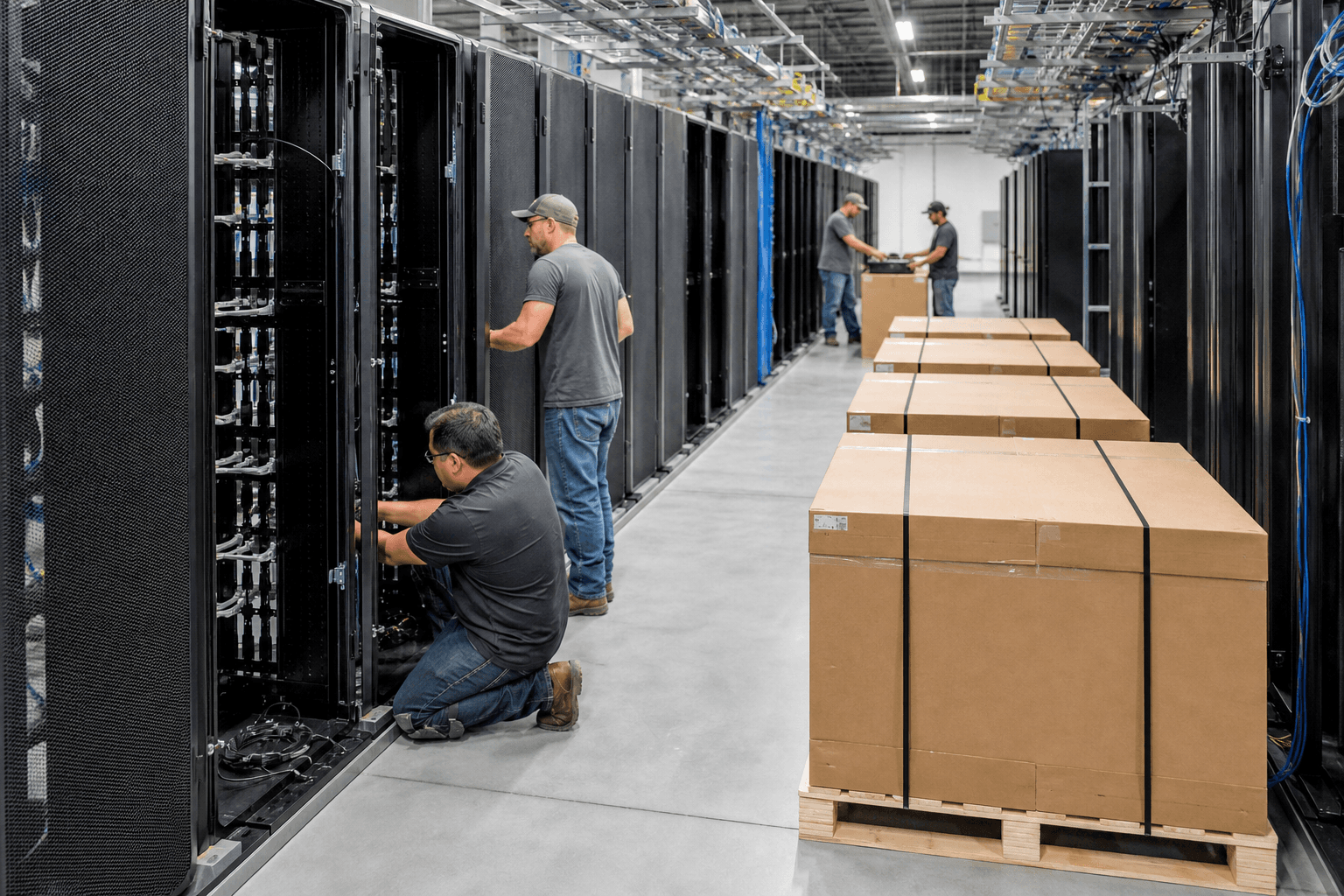

Picture the floor before the press release becomes revenue. Racks have to arrive. Networking gear has to match the cluster design. Storage, integration services, warranty terms, power distribution, cooling, software orchestration, and acceptance testing all have to line up.

The $1.6 billion purchase price covers GPUs, servers, storage, networking, ancillary equipment, integration services, and warranties, according to the company. That list matters because it is the difference between buying chips and selling a cloud service.

Investors are still tempted to talk about AI infrastructure as if the bottleneck is only Nvidia supply. That was true enough for the first wave. But the second wave is messier.

The constraint has shifted into execution:

- Can the operator secure equipment without paying away the economics?

- Can the site absorb the hardware on the promised calendar?

- Can financing bridge the gap between shipment, commissioning, and customer revenue?

- Can the cloud contract survive the awkward period when costs are real but capacity is not fully earning?

This is why IREN's payment terms deserve attention. The Dell agreement is structured with payments after delivery, and IREN said it is advancing GPU financing in connection with the purchase. That is not a footnote. It is the working capital engine under the AI cloud story.

The balance sheet now has to do something more subtle than fund a data center. It has to fund a conversion: hardware order into installed cluster, installed cluster into contracted usage, contracted usage into annualized revenue.

IREN says the Nvidia AI cloud contract is expected to raise annualized run-rate revenue from $3.7 billion to $4.4 billion once commissioned. That $700 million step-up is the prize. The catch is that the prize depends on a schedule, not just a purchase order.

This is the part casual readers miss about AI infrastructure. The winners will not simply be the companies with the boldest megawatt maps or the largest press-release number. They will be the ones that can compress the dead time between capital commitment and billable compute.

For Dell, the deal is another sign that AI server vendors are selling more than boxes. Dell is being pulled into a role closer to industrial project partner: hardware, integration, warranties, and timing all bundled into the customer's revenue plan.

For Nvidia, it shows why the AI ecosystem is increasingly vertical. Nvidia needs cloud capacity for its own internal AI and research workloads. IREN needs Nvidia demand to justify infrastructure scale. Dell needs large, repeatable AI factory orders. The whole stack is starting to look less like spot-market hardware purchasing and more like a financed construction chain.

That does not make the story risk-free. It makes the risks more concrete.

If commissioning slips, the math changes. If financing tightens, the schedule gets more expensive. If customer demand shifts from training clusters to cheaper inference capacity faster than expected, the useful life of today's hardware assumptions gets tested. If newer GPU platforms reset pricing, yesterday's capacity reservation can become tomorrow's margin debate.

None of that means IREN is wrong to move aggressively. In a market where AI capacity is scarce, hesitation has a cost. The company is making a reasonable bet that committed demand plus controlled infrastructure is worth the execution risk.

But the investment question has changed.

The old question was whether AI demand was real. IREN's Nvidia contract gives a pretty direct answer.

The new question is whether AI cloud operators can make time behave like margin. Every month shaved from procurement, installation, and commissioning is not just operational discipline. It is revenue pulled forward, financing risk reduced, and customer trust preserved.

That is why a $1.6 billion Dell order is more than a supplier announcement. It is a clock starting.