Ooma's AirDial Growth Turns Copper Retirement Into An SMB Compliance Budget

TL;DR: Ooma's latest quarter is not just a small-cap cloud communications story. The sharper read is that copper-line retirement is turning old elevator phones, alarm panels, and backup business lines into a recurring compliance budget. Ooma reported 25% year-over-year revenue growth to $81.1 million for the quarter ended April 30, 2026, but the business line worth watching is AirDial, because POTS replacement sells into building operations before it sells into IT fashion.

##What Ooma's Quarter Says About Copper Retirement

Ooma is easy to file under "small business phone software." That misses the more interesting budget line.

In the fiscal first quarter of 2027, Ooma said subscription and services revenue reached $74.6 million, or 92% of total revenue, with growth helped by Ooma Business and the December 2025 acquisitions of FluentStream and Phone.com. Management also called out acceleration in AirDial sales and said it expects accelerating market demand for POTS replacement.

The important phrase is not "cloud communications." It is "replacement."

A company buying a better desk-phone system can delay the project. A building owner replacing old copper lines for elevators, fire alarms, security systems, fax machines, and emergency phones has a different kind of problem. The old line gets more expensive, harder to support, and eventually less available.

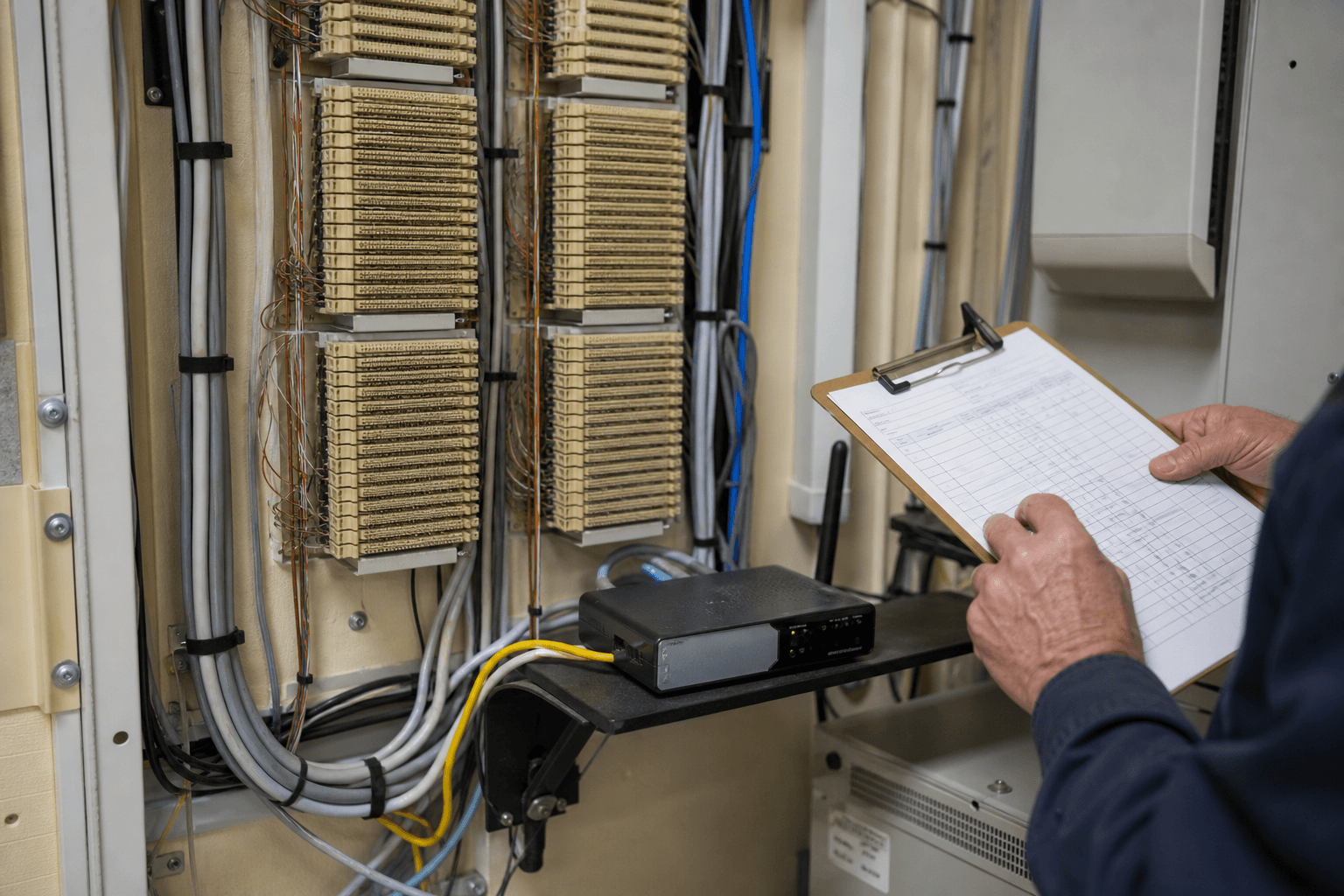

##Why POTS Replacement Is A Facilities Budget, Not A Software Seat

The hidden advantage in POTS replacement is that the buyer often starts with a risk register, not a feature wish list.

Picture a facilities manager standing in a telecom closet with a clipboard, a carrier bill, and a row of copper punch-down blocks that nobody wants to own anymore. The question is not whether the new system has a prettier dashboard. The question is whether the elevator phone, fire panel, and alarm line still work when the old carrier service is retired or repriced.

That turns a communications product into a compliance and continuity product.

#Why the buyer is not always the CIO

The purchase can run through facilities, property management, security, finance, or a reseller that already handles building systems. That matters for sales motion.

An IT buyer may compare UCaaS features. A facilities buyer compares interruption risk, inspection requirements, site rollout pain, and the embarrassment of discovering a dead emergency line during an audit.

The budget is small compared with a cloud migration, but it can be stubborn. Once a building replaces a critical analog line, the customer is buying monitoring, connectivity, hardware support, and a service relationship that is painful to revisit every quarter.

##Where The Regulatory Tailwind Shows Up

The FCC has been pushing the U.S. telecom market away from aging copper networks. In March 2026, the agency said it would vote on rules to streamline copper retirement and "free up tens of billions of dollars annually" for upgraded networks while preserving public-safety connectivity, including changes around network change disclosures and Section 214 discontinuance applications.

That does not automatically hand Ooma a market. It changes the urgency around the inventory.

Companies that ignored analog lines for years now have to answer basic operating questions:

- Which locations still depend on copper?

- Which lines support alarms, elevators, gates, modems, or emergency phones?

- Who signs off when a replacement passes the inspection standard?

- Which vendor handles monitoring, failover, support, and billing after installation?

This is why a POTS replacement vendor can look dull and still sit close to a real business-model shift. The old network is not disappearing as a headline. It is disappearing as a maintenance obligation.

##Who Wins If The Boring Line Item Compounds

Ooma's first-quarter release showed the attractive part of the model: subscription revenue carried almost all of the quarter's revenue base, while product and other revenue stayed much smaller. The company also guided fiscal 2027 revenue to $326.0 million to $328.5 million, which makes the mix question more important than the headline growth rate.

#The hardware is the entry ticket

AirDial still involves devices, installation paths, and channel execution. That is not as clean as pure software.

Ooma's own fiscal 2026 Form 10-K says market acceptance for POTS replacement products such as AirDial depends on compliance with standards including NFPA 72, UL 864, and ASME A17.1B. It also warns that the POTS replacement market is relatively new, has long sales cycles, and includes competitors such as Verizon, Granite Telecommunications, MetTel, AT&T, and Napco Security Technologies.

That is the trade. The market is real because the workflow is painful. The market is hard because the workflow is painful.

##What Investors Should Watch Next

The easy mistake is to treat Ooma's quarter like another communications-software print. Revenue up, EBITDA up, acquisitions integrated, move on.

The better test is whether AirDial can turn copper retirement into repeatable distribution.

Watch three things:

- Whether AirDial growth stays visible after the initial wave of urgent replacements.

- Whether reseller and channel partners can make site audits cheaper to sell.

- Whether product gross margin improves as hardware shipments scale instead of becoming a drag.

Ooma does not need to become the winner of all business communications to make this line matter. It needs to become a trusted replacement vendor for ugly analog use cases that customers would rather stop thinking about.

That is a smaller ambition. It may also be a better one.

#FAQ

What is the main business implication of Ooma's AirDial growth?

AirDial turns copper-line retirement into a recurring facilities and compliance budget. The value is not just phone service; it is continuity for emergency, alarm, elevator, and building systems that cannot simply go dark.

Why does copper retirement matter for investors?

Copper retirement can pull demand forward because customers eventually have to inventory and replace legacy analog lines. The investor question is whether vendors like Ooma can convert that forced migration into durable subscription revenue rather than one-time hardware sales.

What is the biggest risk to the thesis?

The risk is execution. POTS replacement has long sales cycles, compliance requirements, reseller dependence, and large telecom competitors, so demand can be real while still being expensive to capture.