The AI Trade Is Moving Into the Supplier Catalog

Open a small-cap tech screen right now and the glamour is gone.

You do not start with Nvidia. You start with companies most people have never heard of: VIAVI, MaxLinear, Ultra Clean, Ichor. The AI trade is no longer just paying up for the landlord of the boom. It is moving down the hall to the suppliers with clipboards, test gear, tubing, and purchase orders.

That matters more than the rally itself.

When money starts chasing this layer of the stack, the market is making a very specific claim: hyperscaler AI spending is no longer being treated like a story about future ambition. It is being treated like a real procurement cycle that has started to leak into the boring parts catalog.

Reuters reported on May 27 that the Invesco S&P SmallCap Information Tech ETF has taken in $49.7 million so far this year after four straight years of outflows. The S&P 600 small-cap tech index is up almost 54% in 2026, far ahead of the S&P 500 technology index's 20.1% gain. That spread is the widest since before 1995.

People will call that democratization. I think that is the wrong word.

This is not the market discovering a thousand fresh AI product winners. It is the market pricing the subcontractors.

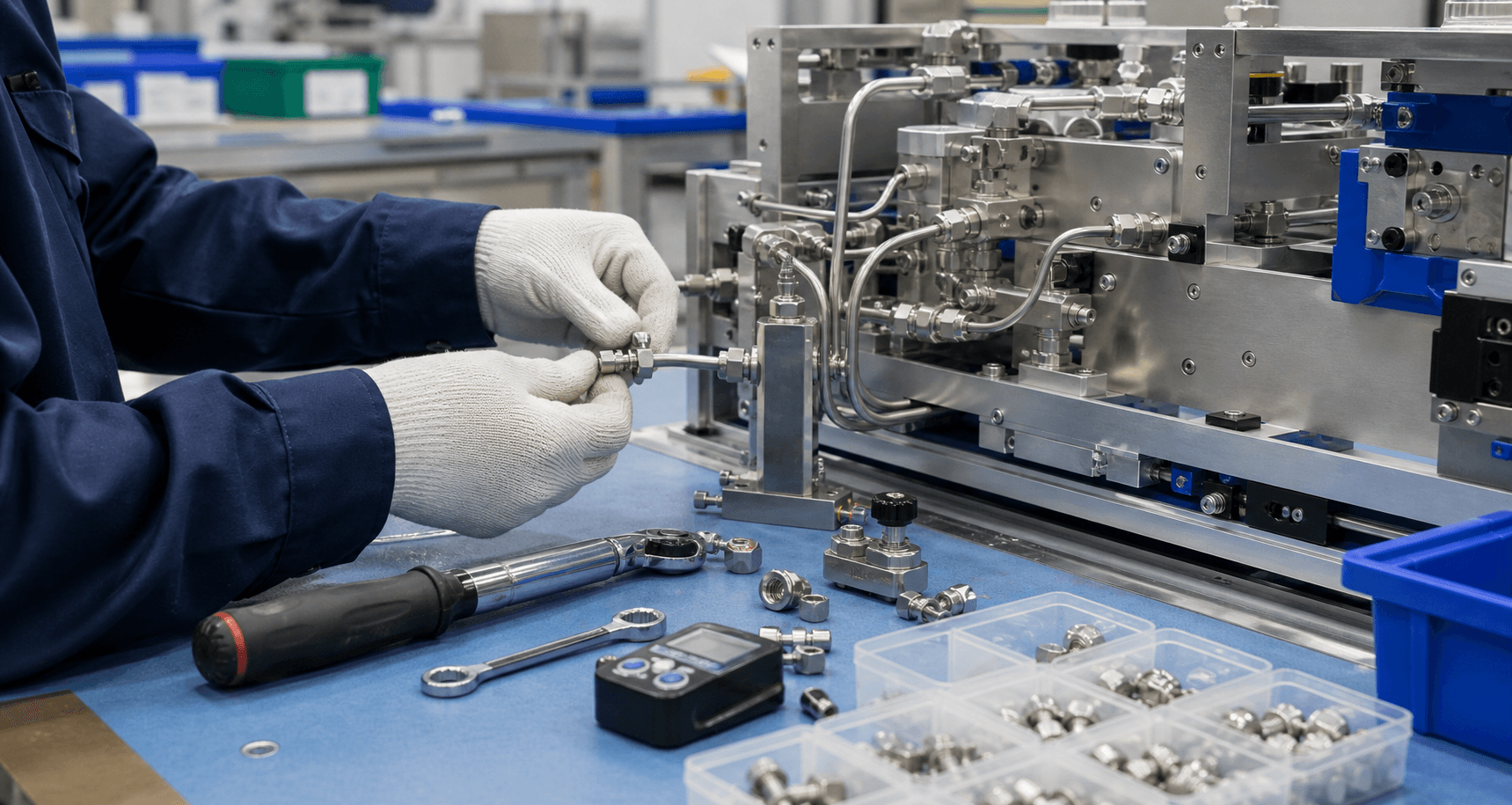

Look at the names Reuters highlighted. MaxLinear makes connectivity chips. VIAVI sells network test and optical products. Ultra Clean sits inside semiconductor tooling. Ichor builds fluid-delivery subsystems for chip equipment. These are not glossy end-user AI stories. They are the companies that get busy when somebody upstream has already decided to spend real money.

MaxLinear's own first-quarter release made the point in plain numbers. Revenue rose 43% year over year to $137.2 million. That is not a meme-stock statistic. That is what happens when optical connectivity around AI data centers starts moving from design-win language into volume.

Ichor's release was even more revealing. First-quarter revenue rose to $256.1 million, up 15% sequentially. Management said it had been ramping labor and pre-positioning inventory so it could meet accelerating customer delivery timelines. In the cash flow section, the company disclosed a $20.5 million inventory increase and a $22.6 million rise in accounts receivable.

That is the real AI buildout, and it does not look like a keynote.

It looks like someone ordering ahead, someone extending terms, someone trying not to miss a ship date, and someone else accepting a weaker near-term cash profile because the line has to keep moving.

The overlooked signal in this small-cap rally is not breadth for its own sake. It is that investors are beginning to reward companies whose job is fulfillment rather than invention.

That is bullish in one important way.

If capital is moving from the megacap GPU names into optical links, test gear, wafer-fab subsystems, and component makers, then the market is saying the demand is real enough to propagate beyond the headline vendors. AI capex is not just supporting valuations at the center. It is creating work orders at the edge.

But there is a second message, and it is less comfortable.

This supplier layer is where the AI trade gets more balance-sheet sensitive. Small-cap hardware companies do not live on narrative alone. They live on inventory turns, receivables, customer concentration, supplier leverage, and debt markets that can get expensive fast when yields rise.

Reuters noted that some investors see speculation outrunning fundamentals in parts of the move. That risk is real. The same small-cap names being rewarded for sitting in the second and third order of AI can get hit much harder if one large customer pauses, if deployment schedules slip, or if financing conditions tighten.

So I would not read this rotation as proof that the AI market has become healthier and broader in some abstract way.

I would read it as proof that the boom is maturing.

In the early phase, investors pay almost anything for the obvious winner.

In the next phase, they start buying the companies that help the obvious winner deliver on schedule.

That is where we are now. The AI trade is moving into the supplier catalog, and that is both a vote of confidence and a warning label.

When Wall Street starts getting excited about the people who manage tubing, optics, testing, and inventory, you are no longer just trading a technology story.

You are trading an execution story. And those are always less forgiving.