PJM's Reform Push Says AI Data Centers Need To Come Hedged

TL;DR: PJM's May 6 market-reform push is a useful reminder that the next AI bottleneck is no longer just chips. In the biggest U.S. data-center corridor, the real scarce asset is firm power with believable financing behind it. That changes the business game: the winners may be less the companies with the loudest AI story and more the ones that can arrive with a hedge, a contract, or their own generation plan.

##The New AI Gate Is Not Compute

The easy way to tell the AI buildout story is to stare at Nvidia orders and server-rack demand.

The harder, more useful way is to look at the conference table where a utility planner, a developer, and a finance person are trying to answer a less glamorous question: who is paying for the electricity if the load shows up before the generation does?

That is where the bottleneck moved.

Reuters reported on May 6 that PJM, the largest U.S. power grid operator, is considering changes to how electricity is bought and sold because data-center demand is outrunning energy supply. PJM serves roughly one in five Americans, and it warned that an electricity shortfall could arrive as early as 2027.

This is not a side issue to the AI trade. It is the part that decides who gets to turn announced capex into real operating capacity.

##Why PJM Is Really Changing The Rules

PJM's own language is blunt. In its May 6 paper, it said data centers can now be built faster than generation can be built to serve them, while capital costs, construction timelines, and policy uncertainty have made new power investment riskier.

That creates what PJM called a credibility trap. Capacity prices spike because the grid needs more supply. Politicians step in because customers hate the bill shock. Investors then wonder whether future price signals will be allowed to hold long enough to justify building the next plant.

The result is a market that is theoretically sending a signal, but not cleanly financing the answer.

#Come hedged or come later

This is why the AI-infrastructure story is drifting away from "who can buy the most chips" and toward "who can show up with power certainty."

Another Reuters report in February said PJM's evolving framework could push new large power users to either bring their own new generation or operate under a connect-and-manage setup that exposes them to curtailment risk when the system is stretched. Analysts told Reuters that this could trigger a wave of direct deals between data-center owners and independent power producers.

That is the key shift. Power is no longer just an operating input. It is becoming an entry ticket.

##What That Means For The Money

If you are a hyperscaler, a neocloud, or a large colocation operator, you now face a more financial market than many people realize.

The project does not only need land, fiber, servers, and customers. It increasingly needs one of these:

- a long-term bilateral power agreement;

- a partner that can bring generation to the site;

- a balance sheet strong enough to absorb curtailment, delays, or transmission costs;

- a willingness to pay for reliability that smaller rivals cannot match.

That is why the most interesting beneficiaries may not be the loudest AI application companies. They may be the power producers, transmission-adjacent developers, and site-packagers that can sell a bundle: land, queue position, electricity path, and contracting discipline.

PJM's updated interconnection fact sheet says more than 800 projects representing 220 gigawatts are being studied in the first cycle of its new process, while about 53 gigawatts already have signed agreements but still face permitting, siting, supply-chain, and local-construction hurdles. In other words, the queue is not the same thing as live capacity.

Investors keep talking about AI demand as if announced demand and usable supply are close cousins. They are not.

##Who Pays If The Buildout Arrives Before The Power

This is where the politics stops being background noise.

Reuters reported on May 11 that Maryland Governor Wes Moore pushed for reforms including long-term power contracts and a requirement that data centers pay for the infrastructure needed to serve them. Reuters also said PJM capacity payments have jumped roughly 1,000% over the last two years.

That is the consumer side of the same story. If AI load arrives first and the financing model stays fuzzy, households and small businesses end up feeling like they are subsidizing someone else's server farm.

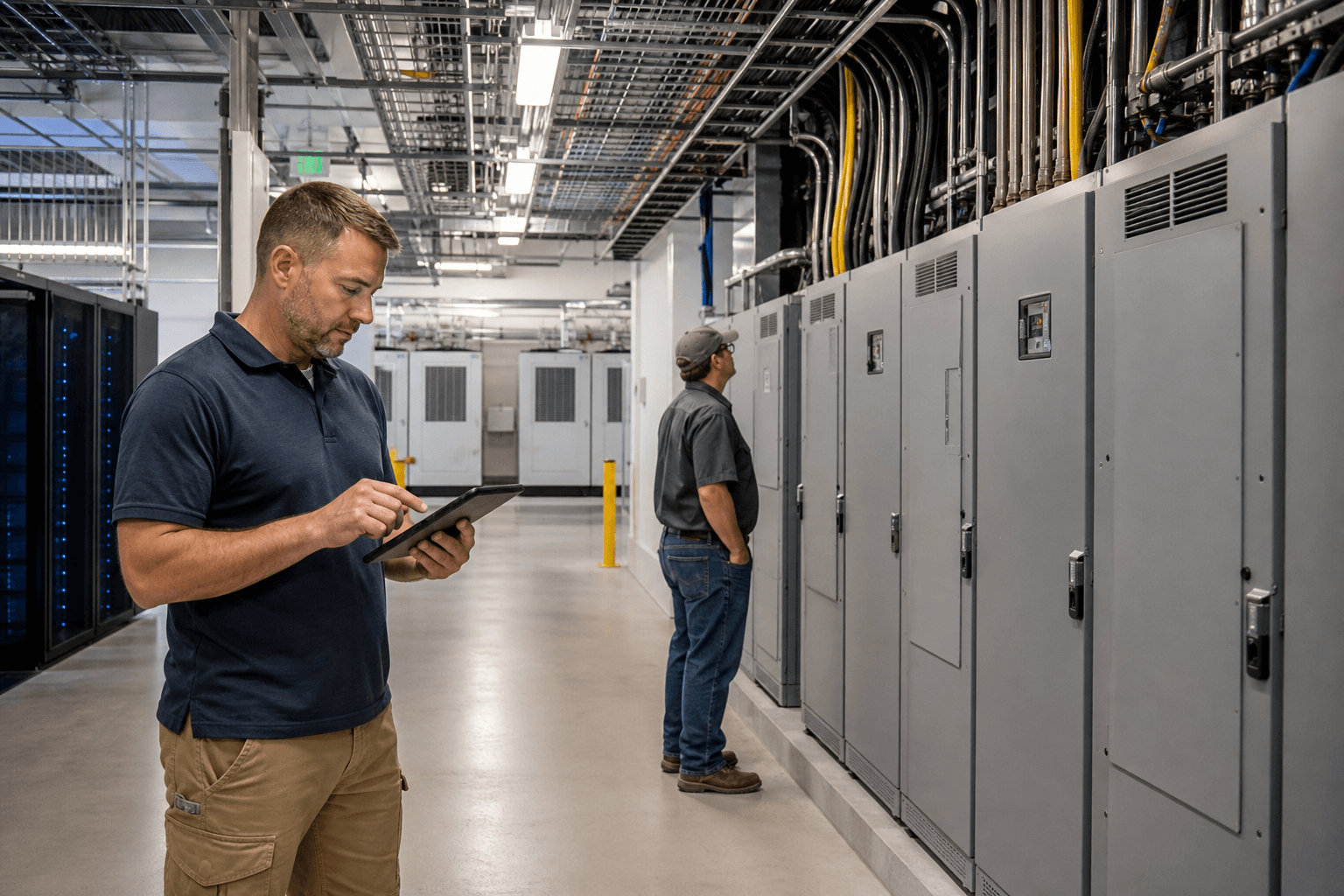

#Power access is becoming a customer-selection tool

Picture the second scene: not a flashy GPU unveil, but a technician in a data-center electrical corridor checking a tablet beside switchgear while someone else studies a closed cabinet.

That scene matters because the AI economy is becoming more physical than the stock market narrative admits. The practical question is not whether demand exists. It is which customer gets energized first, under what contract, with what fallback rights, and at whose cost.

Once the grid reaches that point, power access starts filtering customers by credit quality, contracting sophistication, and political tolerance.

##The Twist In The AI Infrastructure Trade

The popular version of the AI boom says compute scarcity will fade as more chips and servers arrive.

Maybe. But if power arrives more slowly than compute, the scarcity just migrates.

That is the twist casual readers miss. The next durable tollbooth may not be the chip designer or even the cloud platform. It may be the boring layer that can make an AI campus financeable in a stressed power market.

The companies that win this phase will not just promise intelligence. They will package certainty.

#FAQ

Why does PJM matter for AI investors?

PJM runs the largest U.S. wholesale power market and covers the country's biggest data-center hub, so its rules influence which AI projects can secure reliable electricity and at what cost.

What is the main business implication?

The main implication is that AI infrastructure is becoming a power-contracting business as much as a computing business. Firms that can secure long-term electricity or bring generation with them may gain a structural advantage.

Why is this more than a utility story?

It is more than a utility story because it affects data-center development timelines, cloud capacity, project finance, power-producer bargaining power, and ultimately which AI capex announcements can turn into real revenue.