Pyxus' Quarter Says Oversupply Can Still Be A Margin Story

TL;DR: Pyxus' June 4 results matter less as a tobacco story than as a working-capital story. In an oversupplied crop market, the winner is not the company shouting about volume. It is the operator that can buy cheaper inventory, turn it faster, and keep leverage moving down at the same time.

#The Real Product Is Balance-Sheet Timing

There is a boring desk behind every commodity boom and bust. It is not on the farm and it is not on the factory floor. It is the procurement desk deciding how much inventory to buy, how long to finance it, and whether the next quarter will be paid for by margin or by a bank line.

That is why Pyxus' fourth-quarter and fiscal 2026 results are more interesting than they look. Yes, the company reported Q4 net sales up 35.2% year over year, full-year operating income of $162.7 million, record adjusted EBITDA of $226.7 million, and leverage down to 3.52x. But the more important line was management saying it navigated a shift to an oversupply market while still improving working capital and crop costs.

That is the tell. When management wants you to notice oversupply and working capital in the same breath, the quarter is really about inventory economics.

#Bigger Crops Change Who Has The Power

Last year, Pyxus was talking about El Nino-driven undersupply and using a tight market to push through price and volume growth. This year, the company is talking about lower crop costs in South America and an oversupplied market while still pointing to steady demand.

That combination changes the game.

In a shortage market, everyone talks about securing enough product. In an oversupplied market, the business shifts toward:

- who buys inventory at the right moment

- who avoids carrying the wrong leaf too long

- who keeps customers supplied without bloating the balance sheet

That is a different kind of edge. It favors logistics, financing discipline, and local operating judgment more than headline demand forecasts.

#Why Pyxus Looks Better Than A Simple Ag Name

Pyxus calls itself a value-added agricultural company, which is accurate but incomplete. Economically, this business behaves like a global commodity merchant with processing capacity and seasonal financing needs. That means investors should care about the operating cycle at least as much as the income statement.

The June 4 release points in the right direction. Management said full-year results benefited from decreased crop costs, improved working capital, and lower net debt. Guidance for fiscal 2027 calls for sales of $2.3 billion to $2.5 billion and adjusted EBITDA of $210 million to $240 million, which is not a moonshot forecast. It reads more like a company trying to keep the cycle under control than one promising endless growth.

That restraint is healthy.

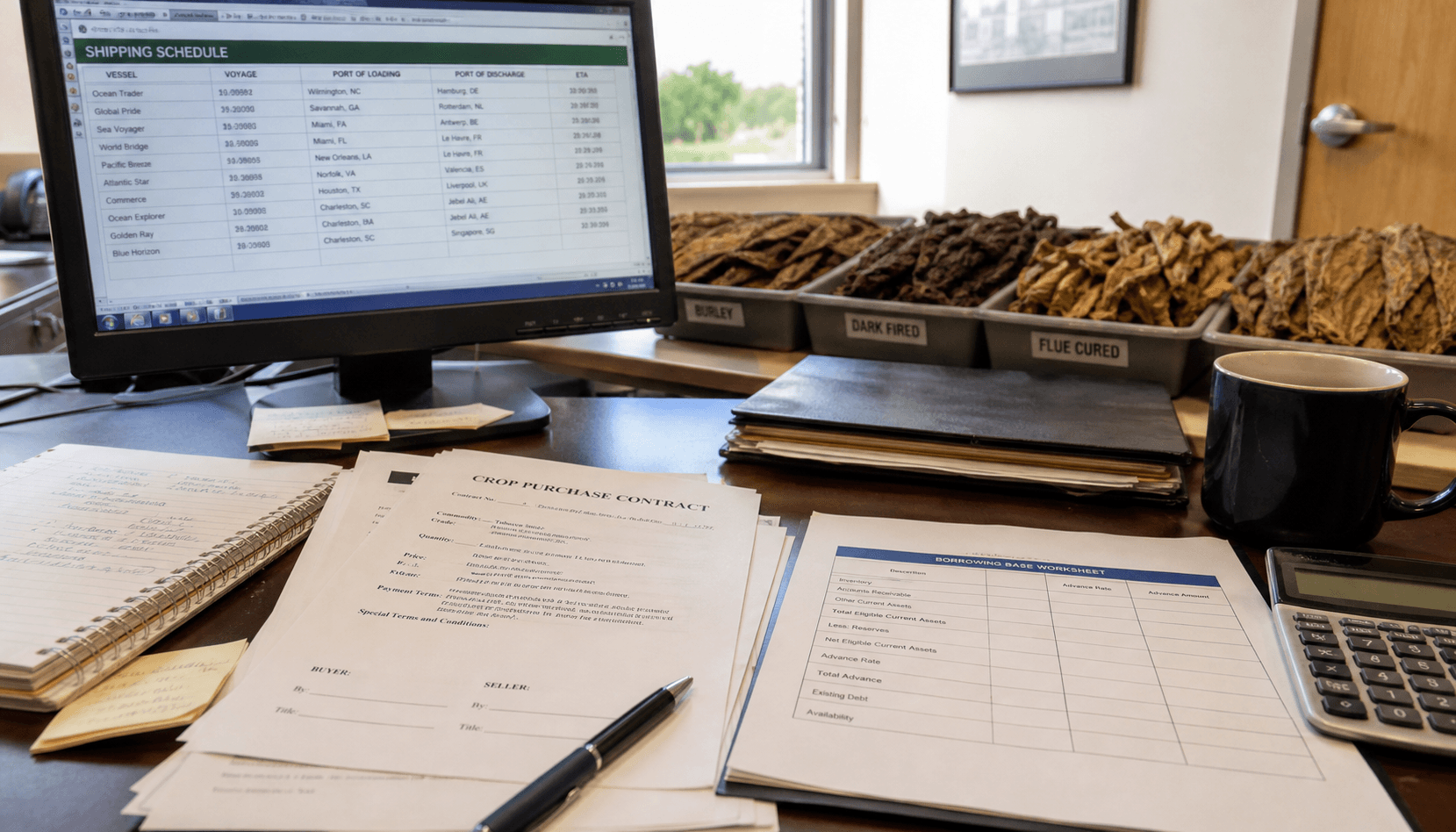

#The Important Scene

Picture the actual operating scene here: purchase contracts on one screen, shipping schedules on another, and a finance team trying to keep seasonal borrowing from eating the margin they just won in sourcing. That is the business. Not the romance of a crop, and not the moral debate around the end market. The commercial puzzle is how to keep inventory moving without letting the balance sheet become the story.

#What The Numbers Suggest

The quarter suggests Pyxus is getting paid for that discipline. If sales are up hard, EBITDA is at a record, and leverage is still falling in an oversupplied market, the company is doing more than enjoying a lucky crop. It is matching procurement, processing, and customer demand well enough to convert cheaper supply into cleaner cash outcomes.

That does not make it a low-risk business. It just means the current edge is operational, not promotional.

#The Broader Lesson For Investors

Investors often treat commodity-linked businesses like simple price bets. That misses where the real money gets made.

For companies like Pyxus, the spread is not only between buying and selling prices. It also lives in:

- how fast inventory converts to revenue

- how much seasonal debt is needed to carry that inventory

- how much operating flexibility management keeps when the crop cycle flips

That is why an oversupply year can still be a good year. Cheaper input costs are only useful if the company has the discipline to buy well, finance prudently, and avoid stuffing the balance sheet with inventory that looked smart one month earlier.

The second-order implication is simple: a lot of old-economy businesses now deserve to be read through a treasury lens. The CEOs may talk about volumes, regions, and customer demand. The real verdict often sits with the CFO, the borrowing base, and the speed of the cash cycle.

#What To Watch Next

Pyxus is not suddenly a glamorous stock. It is still exposed to crop conditions, customer timing, financing costs, and a regulated end market that can change the narrative quickly. But the next useful question is sharper than "is demand okay?"

It is this:

Can the company hold margin and keep leverage moving down if the oversupply backdrop lasts longer than expected?

If the answer is yes, then this quarter was not just a nice earnings print. It was a reminder that in commodity businesses, the best operators do not merely survive the cycle. They turn the cycle into a financing advantage.

#FAQ

Why is this a finance story instead of just an agriculture story?

Because the main signal in the quarter is improved working capital, lower leverage, and better conversion of cheaper crop inputs into earnings. That is balance-sheet execution.

What is the biggest risk after a strong quarter like this?

Inventory discipline fading in a prolonged oversupply market. Cheap supply helps at first, but carrying the wrong inventory too long can quickly reverse the benefit.