Ingredion's Tate & Lyle Bid Is Really A Reformulation Workflow Bet

TL;DR: Ingredion's chase for Tate & Lyle looks like a food-ingredients scale deal on the surface. The more interesting read is that it prices the reformulation desk itself: the teams, customer relationships, and ingredient toolkit that let big food companies cut sugar, tweak texture, defend margins, and still keep products on shelves.

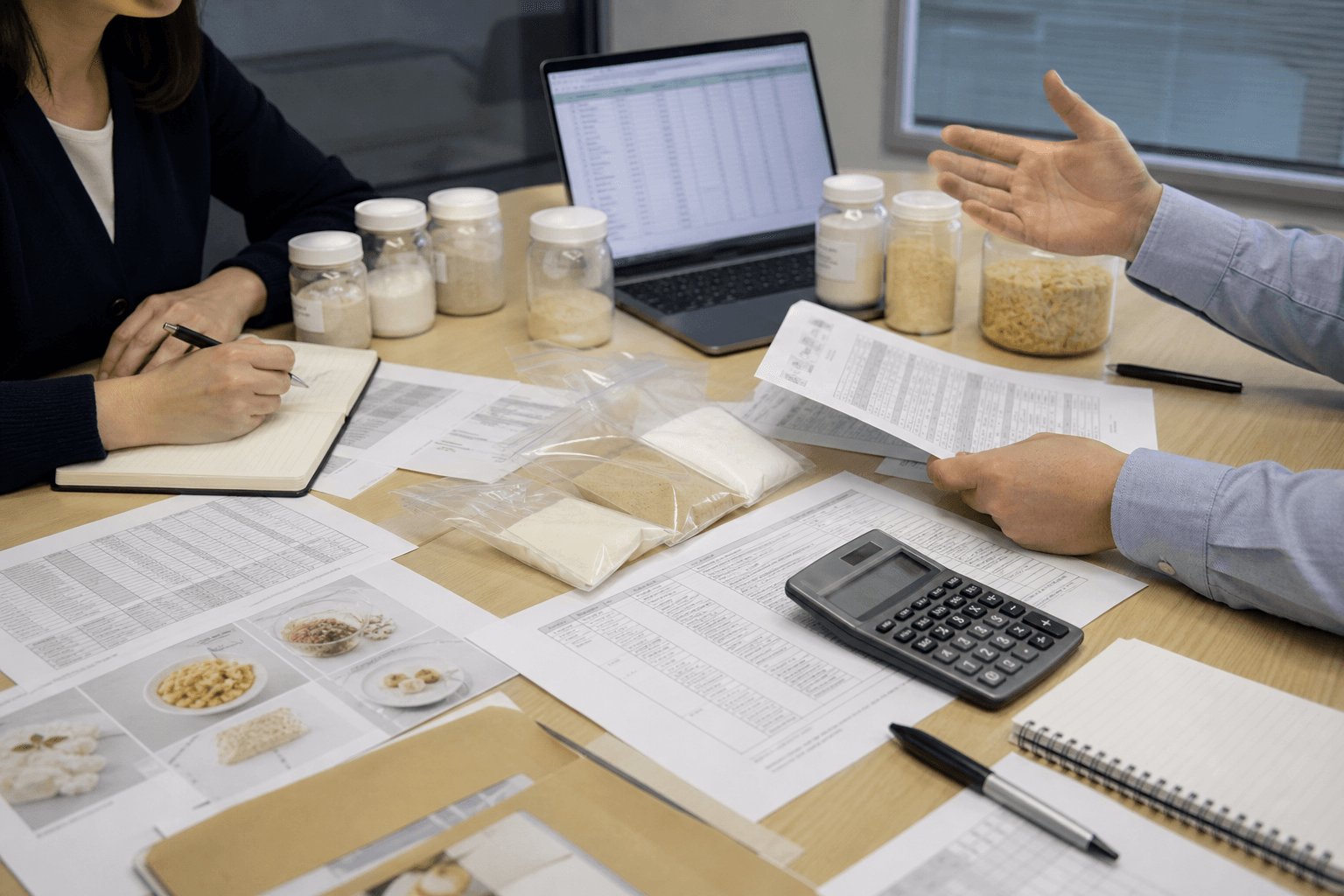

#The Real Asset Is The Workflow

On paper, Ingredion is pursuing Tate & Lyle at up to 615 pence a share, with a June 11 deadline under U.K. takeover rules. That sounds like a standard strategic M&A story.

I think it is narrower and better than that. Ingredion is not mainly buying another ingredients catalog. It is trying to buy a position inside the product-change workflow of global food and beverage companies.

That distinction matters because the most valuable part of this market is not the commodity starch or sweetener sitting in a warehouse. It is the moment when a customer says: we need to remove sugar, hold texture, preserve shelf life, keep the label clean, and not blow up the gross margin.

That is not a commodity transaction. That is an embedded operating problem.

#Why Tate & Lyle Fits That Bet

Tate & Lyle's latest full-year results make clear what Ingredion is really looking at. Tate & Lyle reported about 2.0 billion pounds of continuing-operations revenue for the year ended March 31, 2026, and the company keeps presenting itself around sweetening, mouthfeel, and fortification rather than around bulk ingredient volume.

That is exactly where food manufacturers are spending management attention. Consumer brands are under pressure to hold price, defend volume, and keep reformulating around sugar reduction, protein, fiber, and label claims.

The hard part is that those jobs usually arrive with several constraints at once:

- keep the taste close enough that consumers do not revolt

- keep the label acceptable to retailers and regulators

- keep manufacturing lines running without costly resets

- keep the cost increase below what the brand can pass through

When an ingredient supplier can help solve all four, it stops being just a vendor. It becomes part of the customer's margin-defense stack.

#Ingredion's Own Quarter Explains The Logic

Ingredion's latest quarter also helps explain why this deal makes sense now. In its first-quarter 2026 results, the company said total net sales slipped 1%, while operating income was hit by production problems at the Argo facility and softer volumes in Food & Industrial Ingredients-U.S./Canada.

#The Weak Business Is The Commodity-Like One

Ingredion's U.S./Canada Food & Industrial Ingredients operating income fell 63% year over year in the quarter, to $34 million, according to that filing. That is the part of the portfolio that looks more exposed to operational stumbles and less differentiated economics.

#The Stronger Clue Is In Solutions

By contrast, Ingredion said Texture & Healthful Solutions posted its eighth straight quarter of broad-based net sales volume growth. That is the cleaner signal.

If one side of your business is getting pushed around by plant issues, softer mix, and more ordinary input economics, while the other side keeps winning on formulation-heavy customer demand, you do not need a theory seminar. You need more of the second business.

#This Is A Margin-Control Deal, Not A Food Empire Deal

That is why I do not read this as empire building. I read it as an attempt to move further away from ingredient markets where price and volume do most of the talking, and further toward ingredient markets where customer switching is slower because the supplier sits deeper in R&D, procurement, and regulatory workflows.

Reuters reported on June 7 that Ingredion was in advanced talks to buy Tate & Lyle in a deal valued around 2.7 billion pounds, or about $3.6 billion. The sticker price looks full until you remember what large food customers are actually paying for now: not just inputs, but fewer failed reformulations, fewer awkward label compromises, and fewer margin leaks when recipes need to change.

This is the same reason enterprise software buyers overpay for tools that sit inside approvals and budgets. Once a supplier becomes part of the workflow, the comparison stops being unit price alone.

#What Investors Might Still Be Missing

The easy market take is that Ingredion wants more exposure to healthier ingredients because that is where consumer demand is going. True, but incomplete.

The sharper takeaway is that food inflation and health-driven reformulation are slowly creating a higher-value control layer inside the grocery supply chain. The supplier that can change a formula without wrecking taste, throughput, or margins gets closer to the CFO than the supplier that just ships volume.

#FAQ

Why is this more than a simple scale acquisition?

Because the scarce asset is formulation credibility inside customer workflows. Scale helps, but the economic prize is becoming the team a packaged-food company calls when it needs to rework a product without breaking the P&L.

Why does this matter for U.S. investors?

Because it suggests part of the food sector is being repriced around operating usefulness, not just ingredient exposure. If that is right, investors should spend less time grouping ingredient companies together and more time separating commodity-heavy earnings from workflow-embedded earnings.