Wall Street Is Starting to Buy AI Like Headcount

The most important AI pricing shift on Wall Street is not happening in tokens. It is happening in labor.

This month, FIS and Anthropic did not pitch banks on a prettier chatbot. They pitched a financial-crimes agent that can pull evidence across bank systems and shrink anti-money-laundering investigations from hours to minutes. A day later, Anthropic rolled out 10 prebuilt agents for banks, insurers, asset managers, and finance teams, covering work like KYC screening, audit review, pitchbook drafting, and month-end close.

The easy way to read that is "finance adopts AI." The more useful way is to notice what budget line these products are really chasing. They are not mainly competing for experimental software dollars. They are competing for analyst time, compliance headcount, outsourced operations spend, and all the hidden labor that piles up around regulated workflows.

That distinction matters.

Banks and insurers have never had much trouble buying software. They buy plenty of it. What they hate is adding more expensive people to process repetitive work that still needs audit trails, source checks, escalation rules, and human signoff at the end.

That is why the anti-money-laundering example is so revealing.

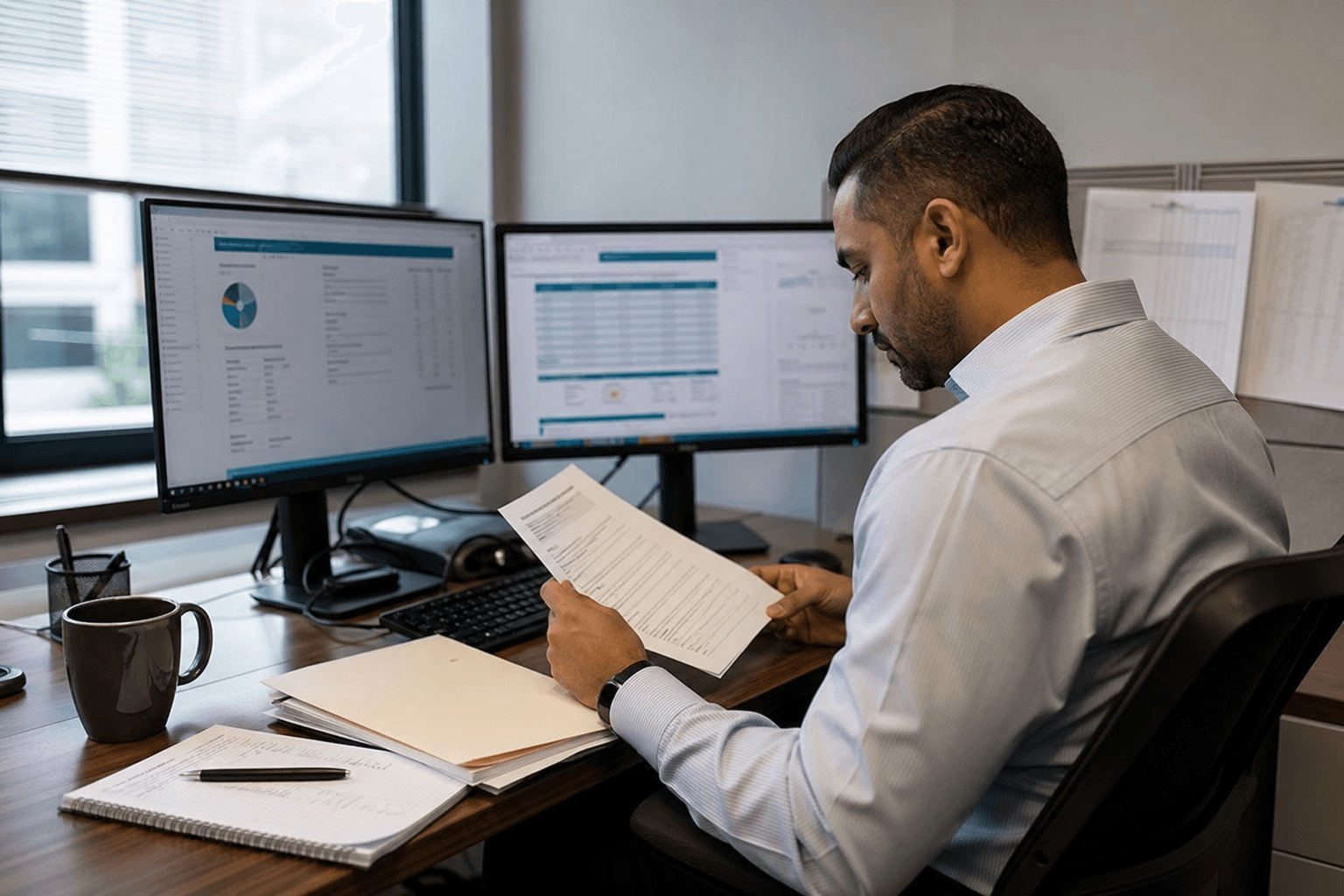

Picture the real scene. An investigator has two monitors open, one for transaction history, one for customer records, plus a case-management queue that keeps growing. The high-cost part of that job is not the final judgment about whether something looks suspicious. It is the evidence assembly: pulling records, matching entities, writing up the chronology, checking policy exceptions, and getting the case ready for a human to decide.

If an AI agent removes half of that prep time, the buyer does not experience it as "better software." The buyer experiences it as fewer hours needed to clear the queue.

That is a labor product.

Anthropic's own product choices point the same way. The company is no longer speaking only in generalities about copilots or model quality. It is packaging finance-specific agents that can be customized to a firm's policies and style. That is a commercial shift from selling raw intelligence to selling workflow compression.

And workflow compression is where the real money is.

In financial services, the highest-friction work often sits in places that are too repetitive for senior staff, too sensitive for full automation, and too expensive to leave untouched. Think sanctions screening, claims review support, risk memos, reconciliations, coverage preparation, valuation backup, policy documentation. These are not glamorous categories. They are exactly where budget lives.

That is also why incumbents like FIS matter more than the public AI conversation suggests.

FIS said it powers nearly 12% of the global economy. That number is not interesting as marketing copy. It is interesting because it explains distribution. In regulated finance, the winner is rarely the company with the flashiest demo. It is usually the company already sitting inside the workflow, already connected to the data, and already trusted enough to survive vendor review, security review, and internal model-risk review.

This is the part casual readers tend to miss. AI in finance is not being bought like consumer software. It is being bought like operating leverage.

That changes the competitive map in at least three ways:

- Model vendors gain value when they can speak the language of a department's backlog, not just benchmark scores.

- Infrastructure and workflow incumbents gain value because they control the last mile between AI output and an audited business action.

- Traditional seat-based software pricing starts to look weak if buyers begin asking a sharper question: how many labor hours, cases, or outside-service dollars did this actually remove?

That last point may be the biggest one.

For years, enterprise software was comfortable charging for access. Per seat. Per module. Per workflow tier. AI is pushing finance buyers toward a harsher standard because the economics are now easier to frame in labor terms. If an agent drafts the first pass of a suspicious-activity report, clears low-risk claims documentation, or accelerates month-end review, management can compare that to salary expense, contractor cost, and backlog reduction almost immediately.

Once that happens, AI spending stops being abstract innovation spend and starts becoming a line-item argument inside the CFO's office.

That is a much more serious buying motion.

It also means some of the most durable AI businesses in finance may look boring from the outside. They may not be the firms with the best public brand or the loudest frontier-model narrative. They may be the firms that can sit inside messy, regulated, expensive workflows and convert model capability into documented throughput.

In other words, the next big AI multiple in finance may not belong to whoever writes the smartest answer.

It may belong to whoever is best at taking a queue of costly human work and making it smaller without breaking the control framework around it.

That is why I think Wall Street is starting to buy AI less like software and more like headcount in disguise.

The minute buyers start measuring these products by cases cleared, hours removed, and teams not hired, the AI market gets tougher and more valuable at the same time.

The real question is not whether finance will use more AI.

It is which vendors get paid when the budget owner stops asking for features and starts asking for fewer people.