Dell's AI Quarter Turns Server Sales Into Deployment Insurance

TL;DR: Dell's quarter was too big to read as another generic AI-server beat. In its fiscal 2027 first-quarter results, the company booked $24.4 billion in AI orders, recognized $16.1 billion of AI server revenue, and lifted its full-year AI server target to roughly $60 billion. The overlooked point is that Dell is increasingly selling deployment insurance: customers are paying not just for compute, but for a vendor that can turn power, cooling, networking, and procurement complexity into a working rack on schedule.

##The Quarter Was Bigger Than A Hardware Story

Dell did not just post a good enterprise-hardware quarter. It posted a quarter that makes the AI buildout look more like an installation business.

The company said first-quarter revenue reached a record $43.8 billion, up 88% year over year. Infrastructure Solutions Group revenue hit $29.0 billion, up 181%. AI-optimized server revenue alone was $16.1 billion, up 757%.

Reuters' summary captured the obvious investor takeaway: Dell raised its annual revenue and profit outlook because the data-center buildout is still pulling hard on AI server demand, with full-year AI server revenue now expected at about $60 billion.

That is the headline.

The better read is that the AI boom is making "server vendor" an incomplete description. Dell is getting paid because customers do not just need boxes. They need those boxes installed, cooled, wired, automated, and live before the budget window or model launch slips.

##Why Deployment Certainty Is Becoming The Real Product

The market still talks about AI infrastructure as if the money mostly belongs to the chip company. That misses where the panic starts after the chips are ordered.

The expensive part of an AI factory is not only buying accelerators. It is getting the whole environment ready for them: liquid-cooled servers, storage, switching, orchestration, private-cloud controls, and the people who can make all of those pieces behave like one system.

That is exactly the lane Dell has been widening. At Dell Technologies World on May 19, Dell laid out a broader "modern data center" pitch that bundled new PowerEdge systems, storage, cyber resilience, and AI-assisted infrastructure automation. The company's argument was not subtle: enterprises do not have time to redesign the data center one component at a time.

That matters because urgency is pricing power.

When a customer is trying to stand up AI capacity fast, the vendor who can compress integration risk starts to look less like a commodity supplier and more like an insurer against delay.

#The hidden bill is project risk

If a hyperscaler or large enterprise misses a deployment window, the damage is not neatly confined to one server invoice.

It can mean:

- expensive GPUs waiting on power or networking

- delayed internal AI rollouts that were supposed to justify the capex

- rushed redesigns around cooling, density, or storage layout

- procurement teams paying more later because they could not lock the whole stack on time

Dell's quarter suggests customers increasingly want one throat to choke for that mess.

##Where This Shows Up In The Real World

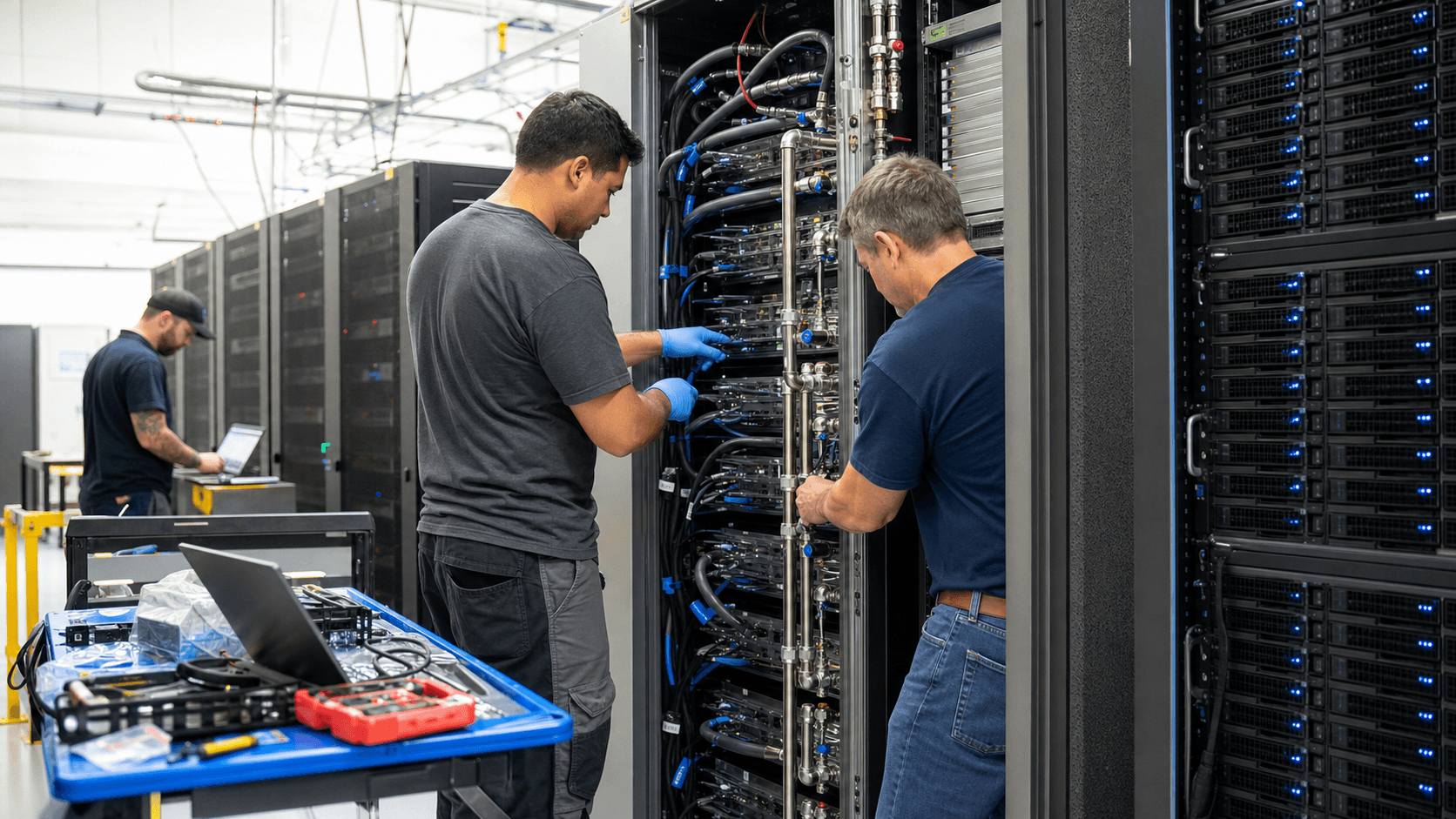

Picture a bright data-center aisle before a new cluster goes live.

Racks are in place. Cabling teams are finishing network links. Cooling assumptions are being checked again because the thermal profile on a dense AI deployment is not forgiving. Someone from finance wants the installation schedule matched to the spending plan, because idle hardware is a very expensive form of optimism.

That scene is where Dell's economics start to make more sense.

The company is not just monetizing a processor cycle. It is monetizing the customer's desire to reduce the number of handoffs between chip vendor, storage vendor, networking vendor, software layer, and deployment team.

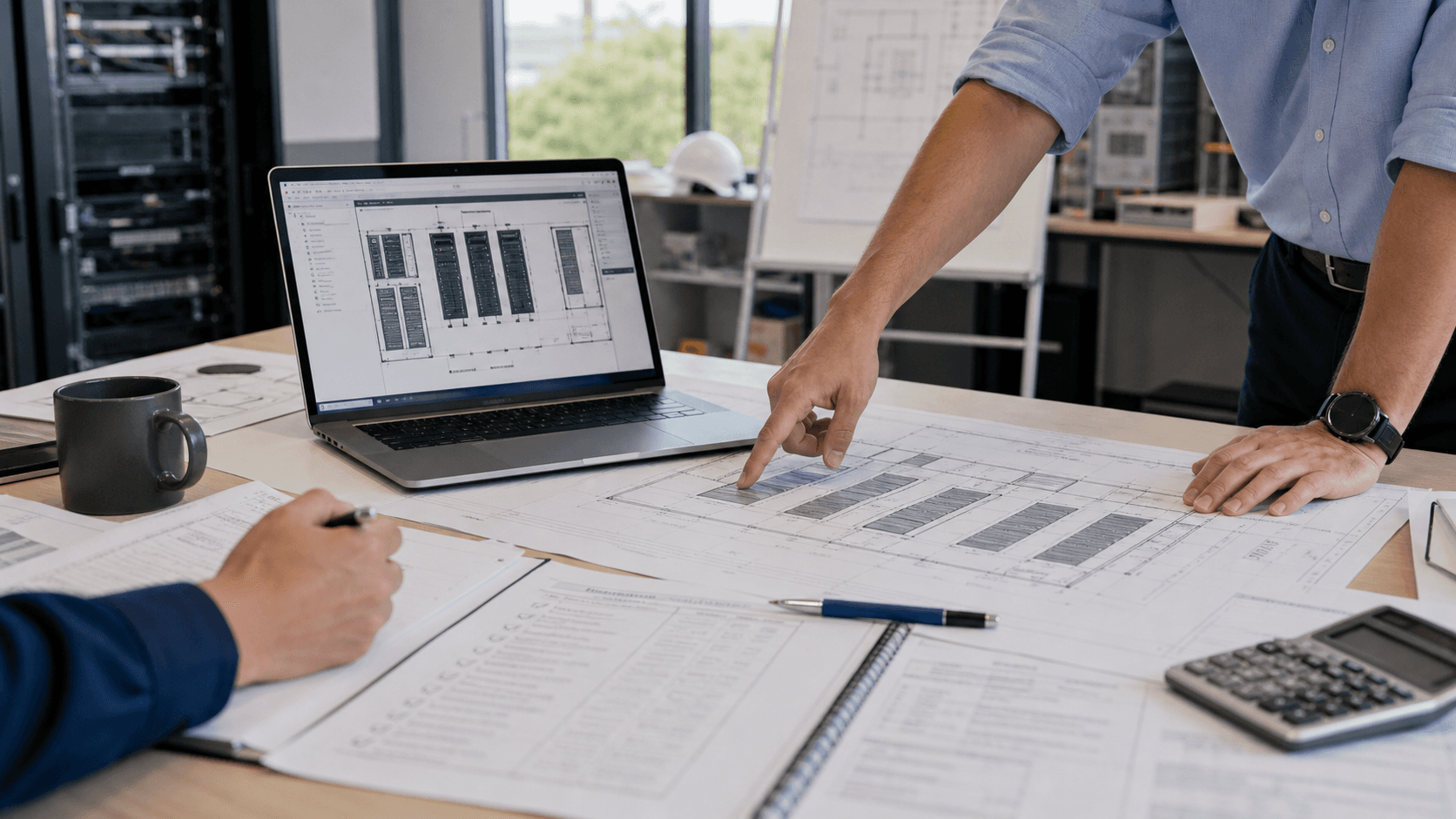

Now picture the second scene: a planning table with rack diagrams, supplier timing, and a power-and-cooling checklist spread across a laptop and printed markups.

This is where the backlog becomes business-model evidence. Reuters noted Dell exited the quarter with a record $51.3 billion AI backlog. That backlog is not just demand. It is a queue of customers effectively outsourcing execution risk.

#This is why the margins may stay better than the old PC-era frame implies

A plain server sale is easier to compare on price.

A full AI deployment is harder to compare cleanly because the value includes scheduling, integration, automation, support, and reduced failure points. Dell's own product pitch has shifted in that direction, from AI factories that span deskside to data center to automation software meant to manage the infrastructure after it lands.

That is not just upselling. It is business-model thickening.

##What Investors May Still Be Underestimating

There is still risk here. This kind of quarter can make every AI infrastructure vendor look invincible for a while.

Dell remains tied to a narrow set of very large customers and to a supply chain that still has memory, networking, and component bottlenecks. Reuters also noted the company has been managing the memory crunch through pricing and supply-chain adjustments, which means execution still matters as much as demand does.

But the bigger point is that the market may still be mislabeling the winner set.

The winners are not only the companies with the best silicon. They are also the companies that can turn silicon into an operating system for deployment.

Dell's latest quarter says that value is getting paid for explicitly now. The AI infrastructure boom is no longer just a chip race or even a server race. It is becoming a race to remove friction between purchase order and productive workload.

That usually looks boring right up until it shows up in revenue. Then it looks like a moat.

#FAQ

What made Dell's quarter stand out?

Dell reported record first-quarter fiscal 2027 revenue of $43.8 billion, including $16.1 billion of AI-optimized server revenue, and raised its full-year AI server revenue outlook to roughly $60 billion.

What is the article's main thesis?

The most important thing Dell is selling is not only hardware volume. It is deployment certainty: the ability to help customers bring complex AI infrastructure online with fewer delays, fewer handoffs, and less integration risk.

Why does that matter for investors?

If Dell is being valued only as a hardware reseller, investors may miss the margin power that comes from bundling installation, orchestration, support, and schedule control into the AI buildout.