Sunshine Silver's IPO Turns A Mine Restart Into A Public-Market Test

TL;DR: Sunshine Silver Mining & Refining priced a 20 million-share IPO at $13.50, putting about $270 million of gross equity behind a planned restart of Idaho's historic Sunshine Mine and related silver, copper, and antimony processing studies. The interesting part is not the silver headline. It is that public investors are being asked to finance the slow, operational middle of U.S. mineral supply: feasibility work, mine infrastructure, permits, processing optionality, and execution risk.

##What Sunshine Silver Actually Sold To The Market

Sunshine Silver Mining & Refining said late June 3 that it priced 20 million common shares at $13.50 each, with trading expected to begin on the New York Stock Exchange on June 4 under the ticker SSMR. The underwriters also have a 30-day option to buy another 3 million shares.

That is an IPO story on the surface. Underneath it, the company is selling something more awkward: a restart plan.

The mine is historic, permitted, and in a familiar U.S. district. But "historic" does not pay contractors, reopen underground development, build a mill, run feasibility studies, or prove that a vertically integrated processing plan can work at commercial scale.

#The useful number is not just the offer price

At $13.50 per share, the base offering raises about $270 million before underwriting discounts and expenses. In its May 26 S-1/A registration statement, Sunshine described intended uses that are very practical: feasibility studies for restarting the mine, building a new mill, developing an antimony plant, restarting a silver/copper refinery, infill drilling, underground development, equipment, infrastructure, project management, exploration, and general corporate purposes.

That list is the story. This is not simply "silver is hot, buy a miner." It is public equity being used as a bridge between a permitted resource and a working industrial system.

##Why This IPO Is A Processing Story, Not A Silver Trade

The lazy read is that Sunshine Silver is an IPO timed for a stronger precious-metals tape. Maybe that helps demand. But the real pitch is about control over the processing chain.

Sunshine says it is one of the few U.S. mining companies with a mine-to-mill-to-refinery platform, with potential onsite silver production eligible for COMEX delivery and major permits required for antimony production. That language matters because the bottleneck in critical minerals is often not finding rocks. It is turning mined material into financeable, specification-ready supply.

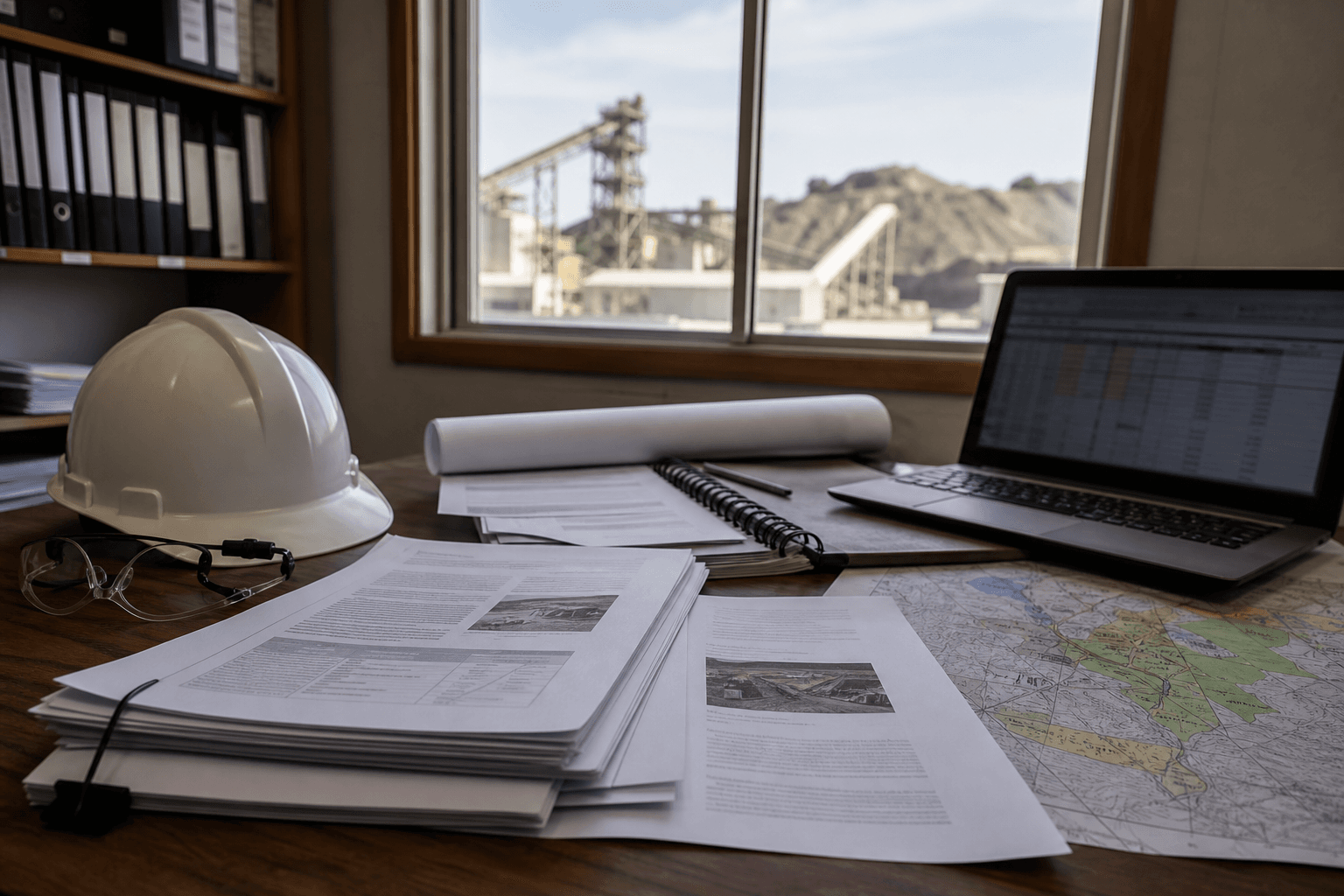

Picture the less glamorous room behind the deal: mine maps on a desk, a laptop model with contractor costs, and feasibility binders that decide whether a public shareholder's dollar becomes a restart schedule or another slide deck.

That is where the equity risk lives.

#Antimony changes the investor frame

Silver gives the IPO a clean headline. Antimony gives it a supply-chain reason to exist.

The USGS 2026 Mineral Commodity Summaries place silver and antimony inside a broader U.S. mineral-supply discussion, and the final 2025 U.S. critical minerals list includes both. Investors do not need to turn this into a national-security slogan. The cleaner point is financial: processing optionality can change who pays for the project, who gets offtake leverage, and what kind of capital becomes available later.

##Where The Public Shareholder Fits

The IPO moves a private restart problem into the public market. That can be useful, but it also changes the scoreboard.

Private mining capital can tolerate long technical work if the sponsor has patience and control. Public equity is less forgiving. It wants milestones, liquidity, and a share price that can absorb bad news from drilling, permitting updates, equipment costs, labor availability, metal prices, or feasibility assumptions.

The handoff looks like this:

- The company gets equity capital before production restarts.

- The investor gets exposure to a permitted U.S. mining and processing plan, not current mine cash flow.

- Contractors, engineers, and equipment vendors become part of the value chain before revenue does.

- Future financing may depend on whether feasibility work reduces risk or merely reveals how expensive the restart really is.

That is a very different contract from buying an operating miner with quarterly production.

##Who Benefits If The Plan Works

If Sunshine executes well, the benefits are not limited to common shareholders.

A domestic silver and antimony processing path could matter to industrial buyers, traders, refiners, and policy-minded capital allocators that want more U.S.-based supply options. The company's location in Idaho's Coeur d'Alene Mining District also gives the story a real operating base rather than a purely promotional exploration map.

But the market should stay disciplined. A permitted mine is not the same as a restarted mine. A refinery study is not the same as refinery throughput. Optionality is valuable only when management can turn it into sequenced, funded work.

##What Investors Should Watch Next

The first trading day may get attention, but the more useful questions come after the ticker starts moving.

Watch whether Sunshine can convert IPO proceeds into concrete de-risking:

#Which milestones reduce uncertainty?

The clean milestones are feasibility progress, infill drilling updates, equipment and infrastructure commitments, mine-development sequencing, and clearer financing choices for the refinery and antimony plant. Vague "strategic" language will not be enough.

#Where can costs surprise?

Mine restarts are cost magnets. Labor, underground development, mill construction, permitting updates, tailings work, and processing studies can all make the original capital story look too tidy.

The twist is that Sunshine's IPO is most interesting if investors do not treat it like a silver chart. The public market is now financing a restart workflow. The metal price may set the mood, but execution will set the bill.

#FAQ

What did Sunshine Silver Mining & Refining announce?

Sunshine Silver Mining & Refining announced the pricing of a 20 million-share IPO at $13.50 per share, with NYSE trading expected to begin June 4, 2026 under the ticker SSMR.

Why does this matter beyond silver prices?

The IPO funds feasibility studies, mine restart work, infrastructure, drilling, and possible silver/copper refinery and antimony plant development. That makes it a test of domestic processing finance, not just a precious-metals listing.

What is the main investor risk?

The main risk is execution. Public shareholders are funding the expensive middle stage between a permitted historic mine and a productive, integrated mining and processing operation.