The AI Chip Race Is Turning Into a Packaging Reservation Business

The most important line in AMD's Taiwan announcement was not about a new chip.

It was the part where Lisa Su said the company would put more than $10 billion into the Taiwan ecosystem to scale advanced packaging, substrates, and manufacturing for rack-scale AI systems. That is the tell. The AI chip race is no longer just a design race. It is becoming a reservation business.

When a chip company starts talking about land, buildings, and manufacturing capacity in the same breath as product launches, the shortage has moved downstream. The scarce thing is no longer only the GPU or CPU architecture. It is the right to move that architecture through packaging lines, substrate suppliers, validation cycles, and volume assembly fast enough to matter.

AMD made that unusually explicit on May 21. The company said the Taiwan investment is meant to expand packaging manufacturing for next-generation AI infrastructure, support its Helios rack-scale platform, and push new interconnect and panel-based packaging work with ASE, SPIL, and PTI. A day later, Su told Reuters that the focus was advanced packaging, substrates, and manufacturing for rack-scale systems, and that some partners needed time to secure land, buildings, and capacity.

That is not normal product-marketing language. That is capacity-booking language.

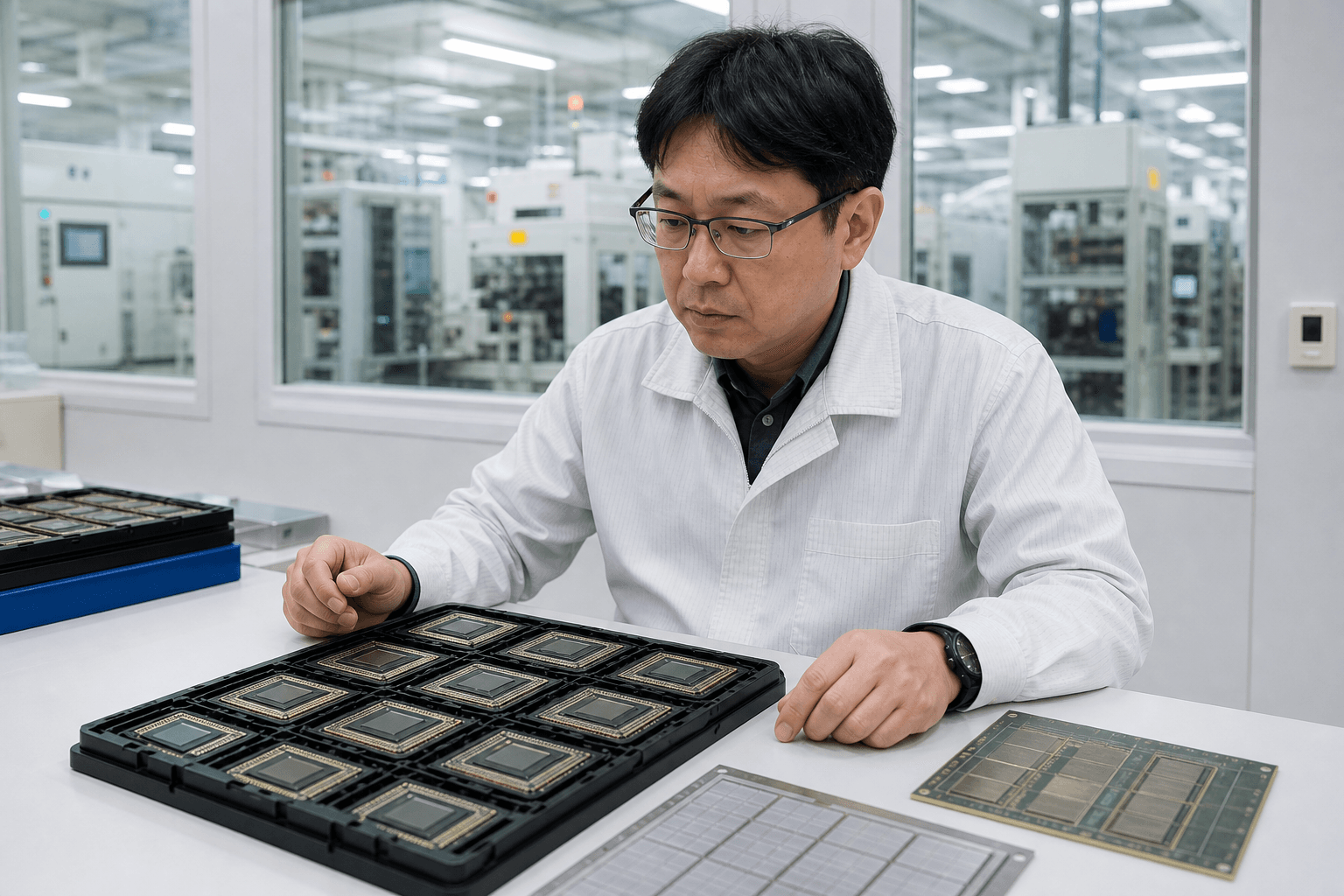

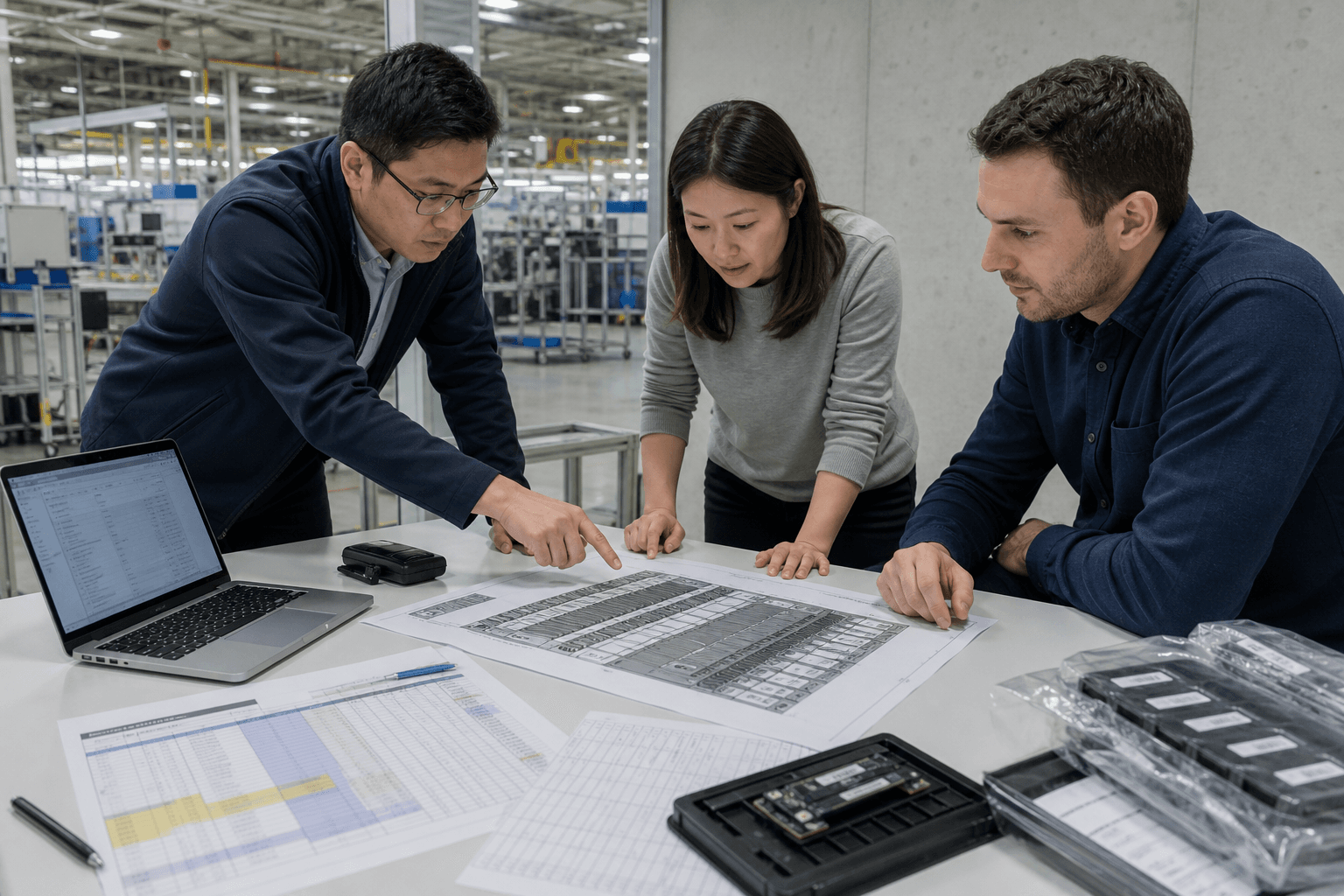

One useful scene here is a packaging room, not a keynote stage. A manager is staring at trays of packaged processors and substrate panels, because the economics of AI now depend on whether those parts can be assembled, tested, and shipped in the right sequence. Another useful scene is the planning table next door, where a team is reviewing rack layouts and factory schedules, because a rack-scale deployment is really a choreography problem disguised as a compute story.

This is why I think investors still talk about AI chips too much as if they were luxury products and not enough as if they were industrial projects.

Industrial projects behave differently:

- They reward the company that can guarantee throughput, not just peak performance.

- They push value toward suppliers that can compress lead times and reduce integration risk.

- They force customers to commit capital earlier, because waiting means losing a slot in someone else's schedule.

AMD is not alone in this. TSMC said this month that it plans to build nine phases of wafer fabs and advanced packaging facilities in 2026. It also said CoWoS packaging capacity is on track for a compound annual growth rate of more than 80% from 2022 to 2027, while AI accelerator wafer demand is projected to increase eleven-fold from 2022 to 2026. TSMC's April revenue was up 17.5% from a year earlier, and January through April revenue was up 29.9%.

Those numbers do not just say "AI demand is strong." They say the bottleneck is being industrialized.

That matters because industrializing a bottleneck changes who captures the profit. Once the market knows packaging is scarce, the winners are not only the chip vendors with the best benchmarks. The winners are the companies that can lock up substrate supply, co-invest with OSAT partners, validate a packaging method early, and promise customers that volume will actually arrive when the data hall is ready.

In other words, AI infrastructure is starting to look less like a merchant semiconductor business and more like a hybrid of project finance and airline seat inventory.

You do not just want a great seat. You want a confirmed seat on the flight that is actually leaving.

That shift also changes the meaning of customer demand. For the last year, the market treated AI demand as a question of appetite: do hyperscalers and enterprises want more compute? The harder question now is operational: who can convert demand into deployed systems without getting trapped in packaging queues, substrate shortages, power constraints, or assembly delays?

That is why AMD's second bet matters so much. Su said the company bet that increasingly complex silicon would need to be broken into smaller pieces and reintegrated through advanced packaging. That sounds technical. It is also a business-model statement. If modern compute has to be assembled from more pieces, then the packaging layer becomes a control point. Whoever manages that layer best gets pricing power, better customer visibility, and a stronger claim on next year's capacity.

This is also where the usual "chip war" framing gets lazy. The market likes clean contests: Nvidia versus AMD, GPU versus CPU, model demand versus cloud spending. Real money is made in the messier layer underneath, where interconnect design, packaging yields, substrate availability, and factory timing decide who can turn a purchase order into a live cluster.

That messier layer is where reservation economics show up first.

Once that happens, the conversation changes. Customers stop asking only which chip is faster. They start asking who can guarantee delivery windows, who can scale with fewer surprises, and who has already paid to keep the line moving.

The next AI premium may not belong to the best chip. It may belong to the company that already booked the packaging slot.