Berkshire's Taylor Morrison Deal Buys Housing Patience, Not A Rate Call

TL;DR: Berkshire Hathaway agreed on May 31, 2026 to buy Taylor Morrison Home Corporation in an $8.5 billion cash deal. The lazy read is that Warren Buffett is making a housing-rate call. The better read is that Berkshire is buying patience: land, balance-sheet endurance, supplier leverage, and the ability to wait out a mortgage market that keeps weaker builders negotiating from the wrong side of the desk.

##What Berkshire Is Really Buying In Taylor Morrison

Berkshire is not buying a spreadsheet that says mortgage rates will fall next quarter.

It is buying a homebuilder that turns land options, community openings, construction schedules, mortgage incentives, and customer deposits into a working-capital machine. That sounds boring. In housing, boring is often the asset.

Taylor Morrison's latest first-quarter 2026 results matter here because a builder is not just valued on homes delivered. It is valued on how much pain it can absorb before it has to cut price, slow starts, or abandon lots.

The public market often treats homebuilders like rate-sensitive cyclicals. Berkshire tends to prefer businesses where time itself becomes a competitive advantage.

That is the point of this deal.

##Why This Is Not Just A Bet On Cheaper Mortgages

The obvious bull case is simple: if mortgage rates ease, buyers come back, orders improve, and builders with land in good markets look smart.

But that framing gives the rate chart too much credit.

Freddie Mac's Primary Mortgage Market Survey has kept the 30-year fixed mortgage in an affordability range that still pressures monthly payments. A buyer does not care that a builder has a good investor presentation. The buyer cares whether the payment clears the household budget.

That is why the real edge is not prediction. It is endurance.

#The builder with the patient owner can negotiate differently

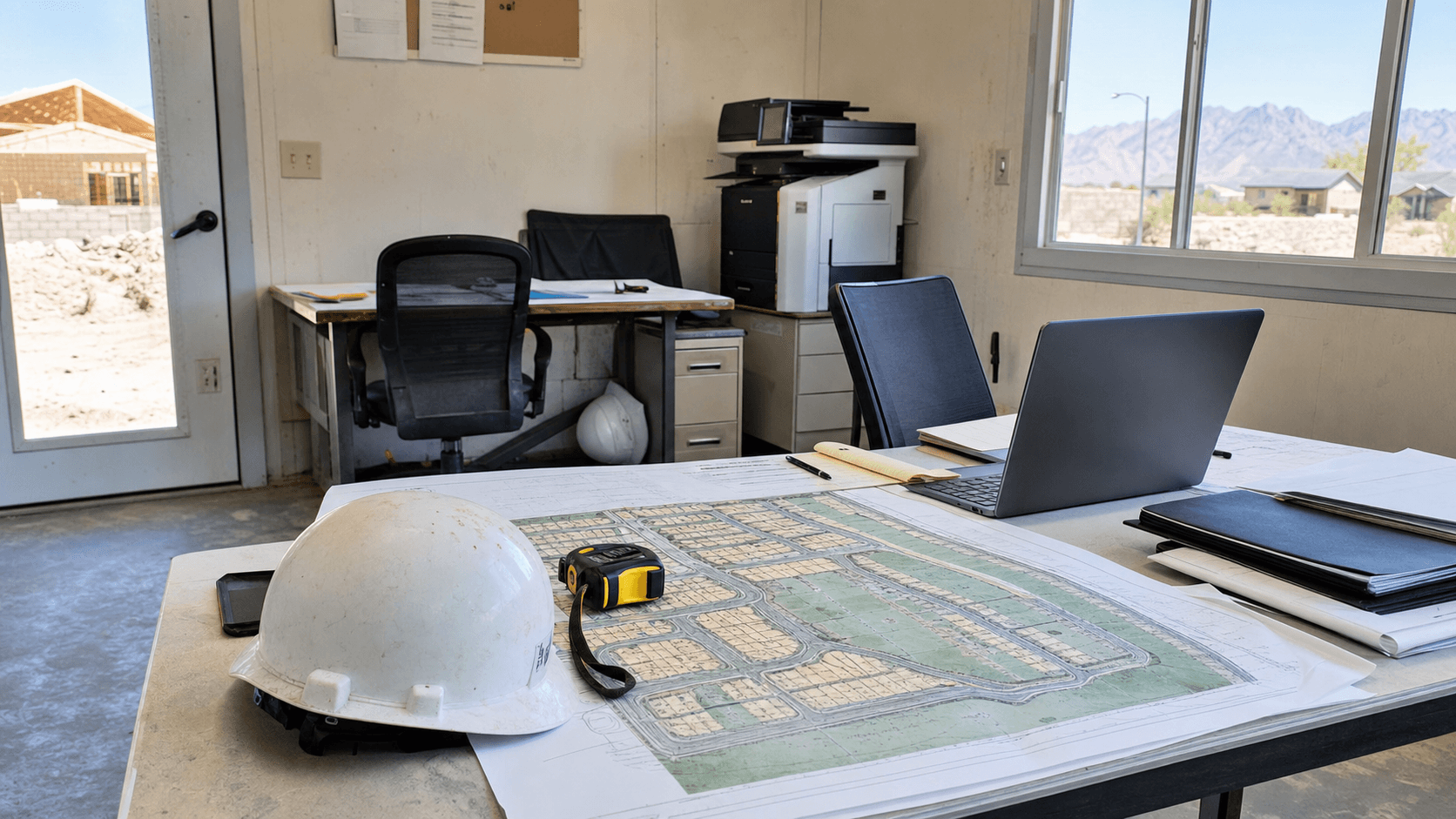

Picture a construction trailer on the edge of a master-planned community. There is a site map on the table, a hard hat by the door, a schedule on a laptop, and a pile of permits that have to move in the right order.

The operating question is not "Will rates be lower by September?"

It is:

- Can the builder hold desirable lots without panic-selling incentives?

- Can it keep subcontractors and suppliers warm without overbuilding inventory?

- Can it use mortgage buydowns selectively instead of turning every closing into a margin giveaway?

- Can it keep opening communities while smaller rivals are protecting cash?

Berkshire's balance sheet changes that conversation. Taylor Morrison's managers still have to execute. But the capital behind them becomes harder to intimidate.

##Where The Housing Market Makes This Useful

U.S. housing has an odd problem: too many households need homes, but the monthly payment keeps blocking demand.

The Census Bureau's new residential sales data shows why investors keep watching builders even when affordability is ugly. New-home supply and builder incentives have become the practical release valve for a market where many existing homeowners are still locked into older, cheaper mortgages.

Existing-home owners can sit still. Public builders cannot.

That difference is why a builder with land, scale, and patient capital can become more important in a stuck market. It can manufacture supply where the resale market is frozen.

The hidden cost is that the builder has to finance the waiting period. Land deposits, model homes, labor coordination, rate buydowns, and unsold specs all consume management attention and cash.

This is where Berkshire fits the story better than a normal strategic buyer. Berkshire does not need Taylor Morrison to look exciting every quarter. It needs the asset to compound through cycles without being forced into dumb short-term decisions.

##Who Loses Pricing Power If Berkshire Is Patient

The deal also puts pressure on a few groups that do not show up in the headline.

Land sellers lose a little leverage when a buyer does not need a perfect capital-markets window.

Smaller builders lose some breathing room if a Berkshire-owned Taylor Morrison can keep showing up for lots, trades, and local relationships while competitors are waiting for financing to loosen.

Subcontractors may like the stability, but stability has a price. A better-capitalized builder can become the preferred customer and still push harder on scheduling discipline.

Homebuyers may get more incentives, but not necessarily lower base prices. Builders have learned that payments can be managed with buydowns, upgrades, and closing-cost help while headline prices stay cleaner.

That is the underappreciated margin defense. The discount does not always look like a discount.

##Why Investors Should Watch The Workflow, Not The Logo

The Berkshire name will get the attention. The workflow should get more.

Taylor Morrison's value now depends on unglamorous execution: community count, absorption pace, cancellation rates, incentive discipline, supplier terms, and land conversion. Those are not press-release details. They are the plumbing of builder economics.

The risk is obvious. If affordability stays stretched for longer, patient capital can still sit inside a slow business. Berkshire cannot repeal mortgage math.

But Berkshire can reduce the chance that Taylor Morrison has to behave like a seller under pressure. In cyclical industries, that difference is often where the money hides.

The deal says something useful about housing in 2026: the best buyer may not be the one with the boldest rate forecast. It may be the one willing to own the waiting room.

#FAQ

Why does Berkshire Hathaway buying Taylor Morrison matter?

It matters because Taylor Morrison gives Berkshire a large operating position in U.S. homebuilding, where land control, incentives, financing patience, and construction execution determine margins.

Is this mainly a bet that mortgage rates will fall?

Not entirely. Lower mortgage rates would help, but the stronger angle is that Berkshire can own a builder through a long affordability squeeze without forcing short-term capital-market behavior.

Who is most affected by the deal?

Homebuyers, land sellers, smaller builders, subcontractors, and housing investors are all affected because a Berkshire-owned Taylor Morrison could keep competing for lots, labor, and closings even when the cycle is uncomfortable.