Dollar General's Raise Turns Discount Retail Into a Mileage Business

TL;DR: Dollar General's June 2 quarter was not a clean vote of confidence in the U.S. consumer. It was a clearer signal that low-income shopping is becoming a trip-compression business. The company raised its 2026 EPS outlook to $7.20 to $7.45 even while keeping same-store sales guidance at 2.2% to 2.7%, and management said higher gas prices, SNAP pressure, and rural budget strain are changing how customers shop. That matters because the winner in this environment is not the retailer with the loudest value slogan. It is the retailer close enough to save a mile, a minute, and a little cash.

##What Dollar General Really Reported

Dollar General's quarter looked sturdy on the surface.

In its first-quarter 2026 release, the company said net sales rose 3.4% to $10.79 billion and diluted EPS increased 12.4% to $2.00. It also lifted full-year EPS guidance while reiterating an aggressive real-estate plan that still includes about 450 new U.S. stores and thousands of remodels.

That is the headline Wall Street sees.

The better signal came from what management and Reuters reported: core customers are under pressure from higher gas prices and reduced SNAP support, with the strain especially visible in rural communities where shoppers are limiting travel and making harder trade-offs.

That changes the frame.

This is not just a cheap-stuff retailer catching a weak consumer. It is a dense-location retailer monetizing the shrinking radius of a stressed household.

##Why The Trip Matters More Than The Basket

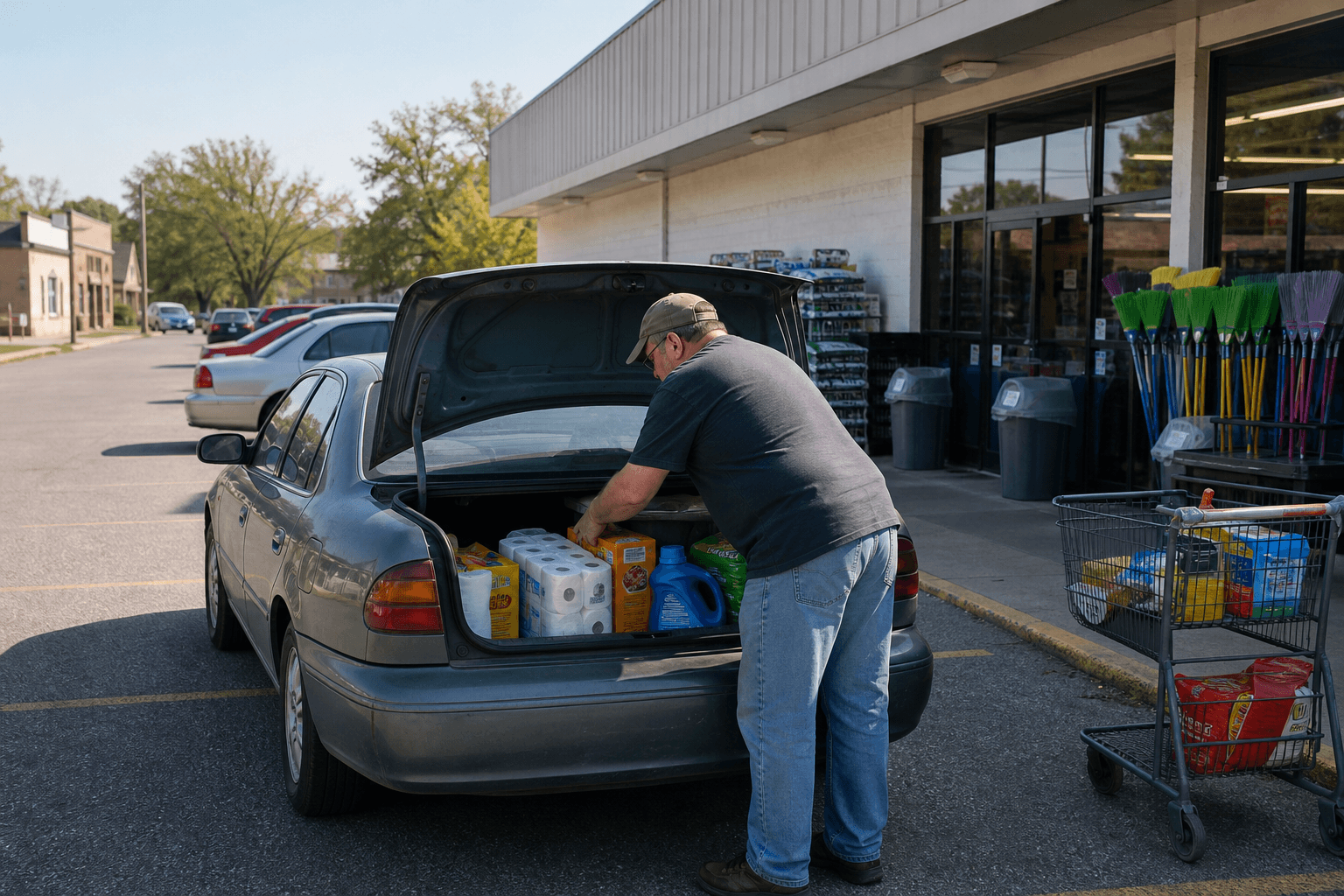

Picture the real scene.

A shopper in a small town does not make one giant weekly optimization decision. She makes a sequence of smaller ones: whether the pickup needs another ten miles, whether the gas tank can wait, whether the store run can cover detergent, cereal, paper towels, and pet food in one stop, whether the extra drive to a supercenter is worth it.

That is where Dollar General's network matters.

Reuters noted that Placer.ai described Dollar General's dense, hyper-local footprint as well positioned to capture short-distance shopping trips. That sounds like a location-statistics point. It is really a margin story.

When gas is expensive and the household budget is tight, the retailer closest to the customer is not only selling cheaper goods. It is selling lower trip cost.

That is why a value chain can hold sales better than the macro mood implies. The customer is not expressing confidence. The customer is trying to reduce friction.

##Why Profit Can Rise While The Customer Gets Worse

This is the part investors often flatten into the wrong narrative.

Dollar General raised profit guidance, but it did not raise its annual same-store sales outlook. That split matters. It suggests the company is protecting earnings through operating discipline more than through a broad consumer rebound.

Reuters said Dollar General is improving margins through supply-chain productivity, store simplification, and tighter inventory management. The company also said its 2026 guidance does not include any potential benefit from tariff refund payments in its earnings release.

That is a useful retail distinction.

There are two ways to post a better quarter in a pressured consumer environment:

- Sell into stronger household demand.

- Run the machine better while staying close to the customer.

Dollar General looks much more like the second case.

That does not make the story weaker. It makes it more realistic.

##What This Says About The U.S. Consumer

The lazy read is that discount retail strength means the consumer is resilient.

The sharper read is that essentials demand is resilient, but the travel radius around that demand is shrinking.

Dollar General's own release lists the pressures plainly: higher fuel and energy costs, healthcare, housing and product costs, higher interest rates, consumer debt levels, and uncertainty around tariffs. Those are not abstract macro variables. They show up as fewer discretionary miles, fewer extra stops, and more insistence that each trip solve multiple household needs at once.

That is why this quarter belongs in a consumer notebook, not just a retail one.

If Dollar General is winning because the shopper wants the shortest functional trip, then value retail is becoming part logistics business, part budget service, and only then a merchandising business.

##What Investors May Be Missing

The underappreciated asset here is not only price.

It is proximity.

In stronger consumer years, store density can look boring. In stressed years, density becomes pricing power's quieter cousin. A nearby store can keep the trip even if it does not win every SKU on headline price.

That is why Dollar General's quarter reads less like a classic turnaround and more like a map advantage.

The next question is uncomfortable: if fuel stays high and subsidy support stays pressured, how much of value retail's earnings durability is actually coming from household stress that nobody should mistake for strength?

#FAQ

Why is Dollar General's quarter more about trip behavior than cheap goods?

Because management and Reuters both pointed to rural shoppers limiting travel and making harder spending trade-offs. That means location convenience is doing real economic work, not just supporting impulse traffic.

Did Dollar General raise guidance because the consumer improved?

Not clearly. The company raised EPS guidance but kept same-store sales guidance steady, which suggests operating discipline and network advantage mattered more than a broad rebound in customer spending power.

What is the main investor takeaway?

Dollar General looks strongest when it functions as a low-mileage household stop. If that remains true, the company's moat is less about promotional theater and more about being the cheapest practical trip.