AI's Next Bottleneck Is the Power Budget, Not the Chip

TL;DR: The AI buildout is starting to look less like a chip race and more like a utility discipline business. When TSMC says energy efficiency is becoming the main constraint on AI chips, it is really saying the value chain is shifting away from raw benchmark theater and toward whoever can turn silicon into a powered, cooled, serviceable machine at scale.

#The bottleneck moved

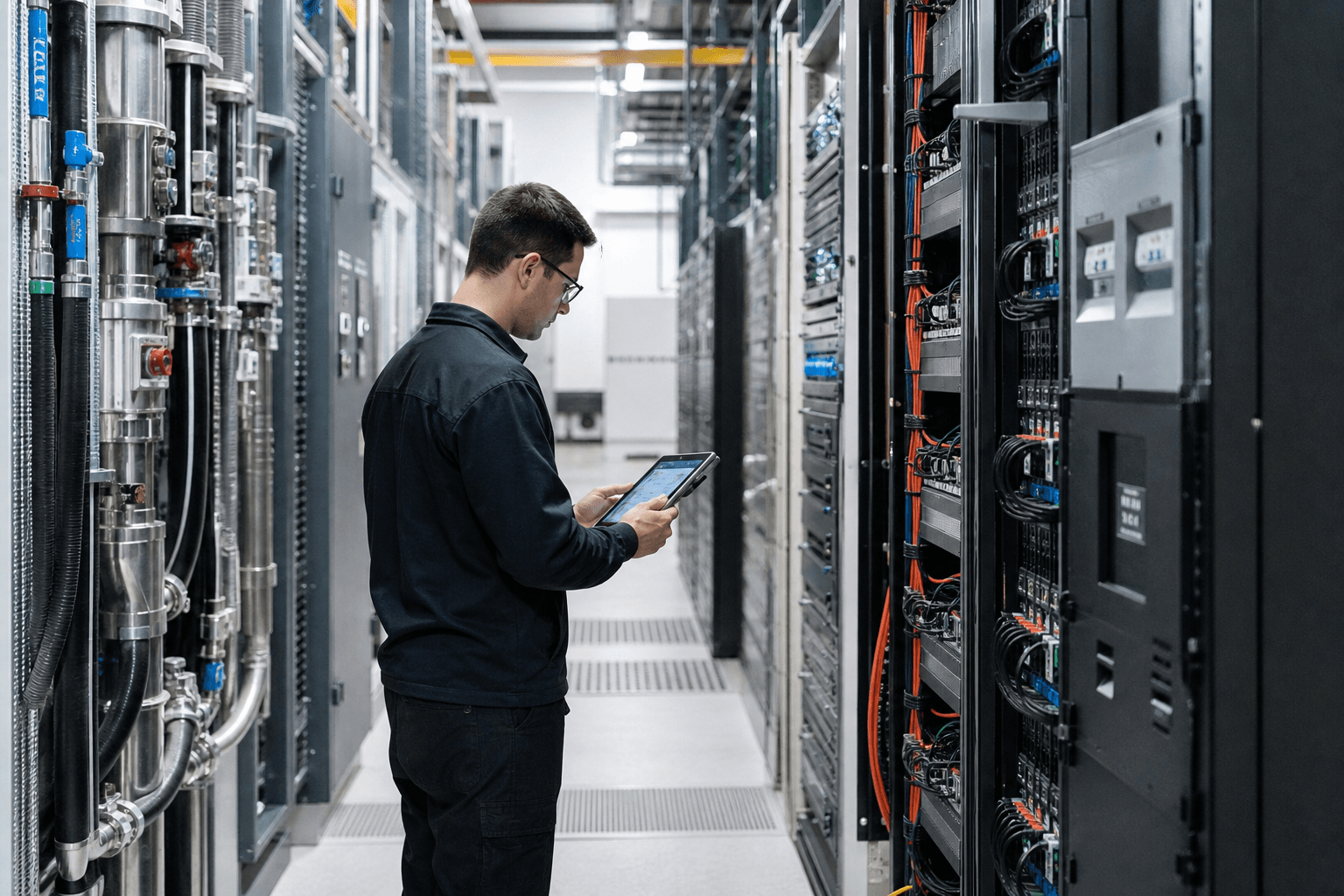

The most revealing AI scene right now is not a keynote stage. It is a technician standing in a bright data-center aisle, checking rack loads while coolant lines snake past server cabinets.

That is where the AI boom gets real. Not at the model demo. Not at the valuation multiple. At the point where somebody has to decide whether the next rack can actually be powered, cooled, maintained, and kept inside a real budget.

This is why TSMC’s Kevin Zhang said this week that energy efficiency, not just computing power, is becoming the main constraint in chip development. The casual read is “chips need to use less electricity.” The more important read is that AI infrastructure is maturing into a deployment business.

#What the money is buying now

The old semiconductor story was easy to tell: more transistors, more performance, higher selling prices.

The new story is messier. AMD’s more than $10 billion Taiwan investment plan is explicitly aimed at advanced packaging, interconnect efficiency, and rack-scale deployment. AMD even framed its Helios platform around multi-gigawatt deployments beginning in the second half of 2026.

Meanwhile, at Computex, Reuters reported that Nvidia’s Jensen Huang said his company could spend as much as $150 billion a year in Taiwan, while Taiwan’s server exports have exploded to $60 billion last year from just $571 million in 2017. That is not just a chip supply-chain statistic. It is evidence that the center of gravity has moved from chips in isolation to full systems.

#Why this matters more than another GPU launch

If power is the hard limit, buyers stop asking only, “Which chip is fastest?”

They start asking:

- Which platform gives me more usable performance per megawatt?

- Which supplier can get enough packaging, cooling, and rack integration done on time?

- Which design lets me expand capacity without rebuilding the room around it?

That changes who has leverage.

Packaging firms matter more. Thermal engineering matters more. Rack builders matter more. Companies that can ship a reliable system inside a real facility constraint start to capture value that used to belong mainly to the chip headline.

#The twist for investors

A lot of AI enthusiasm still treats infrastructure spending as if it were pure demand capture. More models, more GPUs, more revenue. That is directionally true, but it misses the friction.

Once power becomes scarce, not every extra dollar of AI capex buys the same amount of useful compute. Some of it buys workaround costs: better cooling, denser packaging, more complex networking, redesigns, and slower deployment cycles.

That does not kill the boom. It changes the scorecard.

The winners are less likely to be the loudest sellers of peak performance and more likely to be the companies that help customers squeeze more output from the same electrical envelope. In other words, AI is becoming a performance-per-watt market before it finishes becoming a pure performance market.

#Where the margin can migrate

That creates at least three second-order effects.

- Chip design teams get rewarded for efficiency gains that shorten infrastructure payback, not just for bigger top-line benchmark numbers.

- Manufacturing ecosystems with strong packaging and system-integration depth get more strategic pricing power.

- Enterprise buyers gain a new reason to diversify vendors: not just cost, but who can actually fit into the next available power and cooling window.

This is also why Taiwan’s role is widening. Reuters put it well: the question is no longer only who makes the chip, but who can turn it into a powered, cooled, networked, serviceable AI system. That sounds operational. It is also financial.

#The real read-through for U.S. markets

For U.S. investors, the clean takeaway is that AI capex should now be read more like industrial capacity spending than like ordinary software growth. The constraint is physical. The delays are physical. The returns increasingly depend on facility math, not just product excitement.

That means some future upside will show up in less glamorous places than the market expects:

- component and packaging suppliers,

- server manufacturers,

- cooling and power-management specialists,

- cloud operators that can convert capex into deployed capacity faster than rivals.

It also means earnings calls that obsess over demand while saying little about deployment efficiency should sound incomplete.

The AI race is not running out of customers. It is running into the wall socket.

#FAQ

Why is this a business story and not just a semiconductor engineering story?

Because the constraint shapes where capex goes, who gets pricing power, how fast customers can deploy revenue-producing systems, and which parts of the stack capture margin.

Does this weaken Nvidia or AMD?

Not necessarily. It can strengthen the leaders if they control more of the system. But it does mean the market should pay closer attention to packaging, cooling, integration, and deployment economics instead of treating chip demand as a self-executing growth story.